Blockchain in Non-Financial Industries: The Pros and Cons

The technological possibilities of blockchain within different domains seem endless, and it’s an exciting prospect for businesses.

However, before governments, industry leaders, and even the owners of smaller businesses jump head first into blockchain adoption, it is wise to take a step back and take a look at both the huge benefits of the technology, and the challenges that must be faced in that adoption.

No technology solution is perfect for everyone and every circumstance. A reasoned approach will take a look at both sides of this coin and make decisions based upon solid information.

The Benefits of Blockchain

Blockchain has the potential to become an underlying technology for the world’s premier versatile trust network, fostering seamless and secure communication and collaboration between different entities.

There is no question that blockchain technology has amazing potential for almost every sector of the economy. Here are just some of the benefits that public and private sectors need to be considering.

Transparency and Traceability

There are many “eyes” on all transactions that are placed in blocks. And altering any of the recorded and stored data would be merely impossible. Recordkeeping on the blockchain also enables real-time updates and data aggregation from multiple sources, meaning that all the parties receive access to the full picture at one glance.

Transparency ultimately leads to better compliance; reduced administrative costs associated with administering and reconciling data, and diminishes the chances of fraud or corruption in any form.

On the other hand, blockchain technology also allows to seamlessly manage data access and make sure that only authorized parties receive proper access. Private and consortium blockchains often come with full block encryption and AAA capabilities, additionally protecting the transmitted data even if it goes through untrusted networks.

Cost Reductions

Individual and business transactions often involve contracts. These are largely paper and must involve third parties, usually banks, lawyers, and courts. There are plenty of fees involved in using those third parties to “validate” a certain action.

Blockchain eliminates the middleman in these transactions, by codifying them permanently in immutable blocks. Think of all of the contractual relationships, and the possibility of altering documents and fraud. Once a contract is entered into a block, it is a permanent and unchanging document and becomes evidentiary in any legal dispute.

Individual states in the U.S. have already passed legislation recognizing the legal validity of contracts stored in the blockchain, notably Vermont and Arizona. In January of this year, a bill was introduced in the Florida state legislature to do the same. Recognition of such contracts certainly reduces enforcement and legal dispute costs for both individuals and companies.

The benefits of smart contracts can be summed up in the following points:

- Accuracy. All the clauses are enforced and executed automatically, leaving no room for manual mistakes.

- Faster execution and real-time updates. Considering that all contracts are managed and executed automatically, instead of manually, a lot of business processes can happen at a faster pace.

- Reduced costs. Contract management requires less human supervision and intervenience, thus reducing the associated administrative costs.

Fraud and Hacking Prevention

A typical enterprise loses 5% of its revenues to fraud on an annual basis. Because blockchain is immutable and distributed (shared), an individual or group of fraudsters have extremely low chances of tampering the network in any way.

Remember, before a transaction is recorded in a block, all network participants must agree on its validity, through consensus. That transaction is time-stamped and secured through cryptography. A new transaction that amends the original transaction or asset can be added, but the original still stays in place. It is therefore easy to see the provenance and the progression. Consider these uses:

- Counterfeiting is a worldwide problem, whether it is diamonds, clothing, food or pharmaceuticals, etc. Manufacturers/producers of these goods can prove the authenticity of their assets if those goods are placed in blockchain and time-stamped.

- Access to many blockchains is permission-based. This means that those who should have access are provided key codes for entry. This is especially important for medical records when there are so many regulations regarding privacy. Health care providers can access complete patient history records, provide better care, and have the security of knowing that those records have not been tampered with. Further, they can add to those records and know that they are secure and viewable only by those who have permission.

- Educational records, especially transcripts and degrees, have always been the subject of fraud. They are easily created and altered because they are still largely paper in nature. If these records are in a blockchain environment, and permission is granted to those who need to see them (potential employers, other institutions), then those individuals can be assured that they are valid.

More Rapid Transactions/Settlements

The blockchain is a 24/7/365 environment, and transactions are verified and recorded automatically. Without blockchain, transactions are impacted by regulations, protocols, and even time zones. But consider, too, that other industries can benefit from the speed.

- Insurance adjusters can verify claims and add them to the blockchain, eliminating lots of paperwork and bureaucracy at the home office. Claimant payments are then processed more rapidly.

- In the logistics/transportation industries, the sending and receipt of goods can be recorded immediately and tracked/verified through each checkpoint, thus allowing invoicing to occur quickly.

User-Control of Networks

Traditional transactions/records have relied on third-parties “running the show.” With blockchain, users get to run it instead.

Consider the rapid rise of what we now call the sharing economy – companies like Uber and Airbnb. In both of these instances, there is an ownership at the top that controls all transactions and takes their fees. Everything that both of these enterprises do could be done through a couple of smart blockchain agents who develop cooperatives based upon common needs/interests. Thus, users of Uber and Uber drivers would “match” themselves. And the drivers themselves would have a cooperative, with all revenues being shared among members based upon their participation. And blockchain records that participation.

Travelers must rely on government bureaucracies to provide their identity documents and to verify them at various checkpoints during their journeys. And the problems are many – identity theft, counterfeiting, and loss, etc. It’s a big problem. And through it all, people must rely on someone else. Blockchain technology can allow a traveler to establish his identity with accompanying documents, permanently record and store them, and have personal control. No more producing physical ID documents at checkpoints and far less chance of fraud or theft.

Challenges

With all of these benefits, it is easy for businesses and governments to be tempted to jump in quickly. Fortunately, that is not happening, and, instead, various sectors have set up pilot projects to “test” the feasibility of blockchain on a larger scale within their enterprises/domains. And they have certainly met with some challenges that, while not insurmountable, will require additional technological and human solutions. Here are just the most common.

Awareness

Many government agencies, business leaders, entrepreneurs, and institutional heads do not have a full understanding of just what blockchain is. If they have heard of it at all, it is usually in conjunction with cryptocurrencies. To many, this is a mysterious and possibly suspicious digital currency that they are not quite ready to embrace as mainstream.

While financial services sectors have made it their business to study the cryptocurrency markets and their underlying blockchain technology, most other industries are just stepping into this domain.

Interoperability

While large global distributed ledger networks operate their specific way, numerous private and public blockchains appear on the scene with their own unique implementations. Unfortunately, there are still no unified standards for the technology. The competing blockchains lack interoperability to become compatible with the World Wide Web and existing practices.

Absence of common international standards and guidelines creates a problem. For instance, two major healthcare providers have established their own technologies, and those technologies are not compatible with one another. How do patient records get cross-added if and when that becomes necessary? If there were standardization among all healthcare providers, this problem would be eliminated.

These same problems exist with other sectors as well, e.g. insurance, when two companies must work together to settle claimant disputes and validity.

Regulatory Environment

Already, governments are stepping in to regulate the cryptocurrency markets. But they have generally had a “hands-off” policy with regard to blockchain technology. In the U.S., for example, the general feeling is that this is a matter for each state. Some states have taken the initiative to recognize documents, contracts, and stored transactions as have legal weight. Most states have not done so.

The answer probably lies in federal regulations. This creates a level playing field among parties who transact business among multiple states. And more businesses would probably be prone to adopt the technology if they knew there were national regulations and guidelines.

One more example with regard to illegal content. Certain information can be illegal under national legislation. Once imbedded into a blockchain by a malevolent user, the illegal component could put the entire blockchain outside the law since there is no way to delete it due to indelible nature of this technology.

Privacy

In terms of privacy, blockchains dwell upon not anonymity like many may think, but upon pseudonymity. Though we are talking about non-financial applications, the arising issue can be nicely illustrated with cryptocurrency example. If you decided to send a few Bitcoin to your grandma, your identity behind your public key is immediately exposed, and due to inherent transparency your grandma, from now on, can see not only how much you have on your account, but also trace every transaction you made with it before. Same could apply to personal information in insurance or healthcare field.

Another issue is with indelible nature of blockchain data – every piece of information is stored forever. This creates collision with the recent EU General Data Protection Regulation, where the data subjects have the right to change their personal information or entirely delete it (the right to “be forgotten”).

Efficiency and Scalability

Despite the excessive hype around the “heavenly” technology, blockchain networks are relatively slow processing the ever-growing bulk of records. Each node in the network has to keep and update the full copy of all transaction histories doing the same job as any other node, the network bandwidth and processing capacity equals to those of one node. To understand what that means, for instance, network processing speed of Bitcoin blockchain is 7 transactions per second at the most, while “old-fashioned” Visa processes thousands of transactions per second and, if required, can easily scale up.

Energy

Being heralded to become solution to global issues like the global warming, blockchain technology at its current stage consumes ever growing amounts of energy for doing the same portions of job – confirming blocks of transactions and adding them to the chain, thus leaving a massive carbon footprint of its own.

Culture

Adoption of blockchain technology requires a major paradigm shift in thinking. People are used to their paper trails, to their fax machines, and to their own private in-house databases. Many of these same people have had trouble transferring their activities to the cloud.

There is a general unease with what is perceived to be a loss of control over information and data.

The answer probably lies in small pilot endeavors, so that organizational staff can see the benefits and gradually get accustomed to the technology and what it can do.

Security

This is a far more serious issue with private blockchains that provide access only to those with permission. In public chains, identities are encrypted and so far, there has not been a breach. Any organization entering a public chain must ensure that the encryption processes will protect privacy and identity.

With respect to private permission-based blockchains, the security issue really lies with the users and protection of their security key codes. Storing them on personal devices and even on work computers is a big “no-no” for obvious reasons. Most developers recommend that key codes be stored on an external hardware device that is only inserted and used to authorize required transactions. As long as the key codes remain safe, no data hampering can take place.

Just what is the takeaway from all of these pros and cons? It is probably safe to say that blockchain technology looks to be the next big technology disruptor for all sectors of the economy. It holds significant promise for trustful transactions, the immutability of transactions, data, documentation, etc., and will certainly be a much more efficient and secure environment in which all of these things can be stored.

Finding Information

Verifying, encrypting, and adding data to the blockchain is just a routine part of keeping distributed ledger. Actually, this is all what is needed to operate cryptocurrencies. For non-financial industries it is more important to have a possibility to use data in various ways, which means to have a reliable way to find it. This can be achieved through indexing the blockchain into a searchable database. But to make it distributed and function properly, every user has not only to store and continuously update the entire blockchain, but also do the same with a much larger search index being built from it.

Associated Costs

Creating a 100% reliable decentralized database system with immutable audit trail is a tough and costly task. The process of development is much stricter and slower due to dramatic sensibility to even a smallest bug. Agile development methods are totally inappropriate since losing a bit of consistency makes the entire blockchain worthless. There is no way to fix problems on the go.

Maintenance also gets rather costly. Blockchain database needs to be written, checked for consistency, and transmitted thousands of times.

Upgrades are voluntary and resistant to implement. Decentralized public systems require consensus of all players on the network, there is no single authority to force upgrades. Malicious or misbehaving users cannot be banned or kicked out, thus creating another level of difficulty.

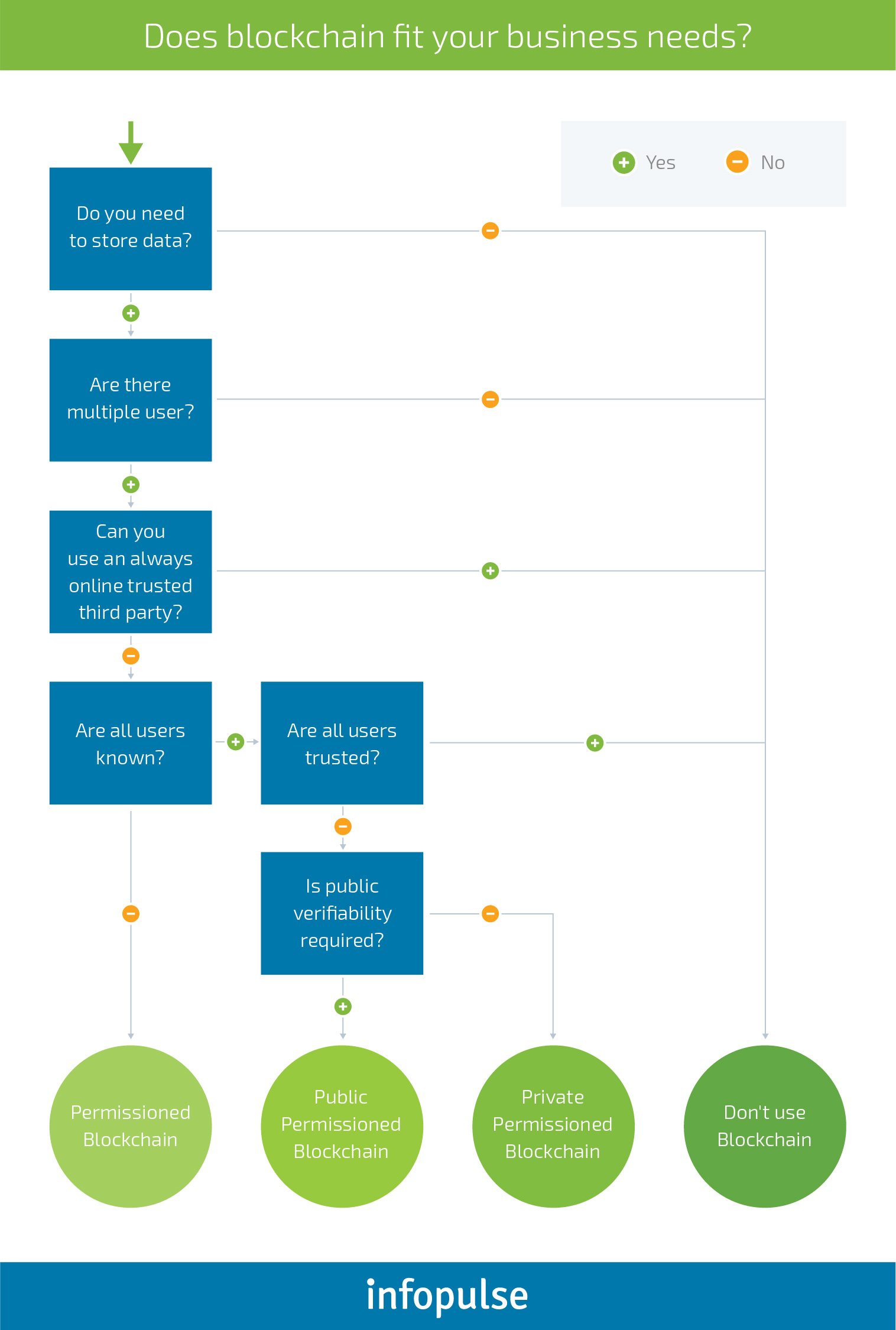

So blockchains are very expensive as compared to centralized databases. The only reason to use blockchains is when decentralization is required, i.e. elimination of the single point of failure or control. Below is a simple scheme to find out whether your organization needs blockchain technology created by Karl Wüst and Arthur Gervais from Department of Computer Science ETH Zurich, Switzerland.

Are there any other challenges? Of course. There were challenges for Henry Ford when he developed his first car, too. Over time, however, as with anything worthwhile, those challenges are met with solutions. Blockchain technology will be no different.

In our next article, we will have a deeper look into prospects for using blockchain in the healthcare sector.

![Pros and Cons of CEA [thumbnail]](/uploads/media/thumbnail-280x222-industrial-scale-of-controlled-agriEnvironment.webp)

![Power Platform for Manufacturing [Thumbnail]](/uploads/media/thumbnail-280x222-power-platform-for-manufacturing-companies-key-use-cases.webp)

![Agriculture Robotics Trends [Thumbnail]](/uploads/media/thumbnail-280x222-what-agricultural-robotics-trends-you-should-be-adopting-and-why.webp)

![ServiceNow & Generative AI [thumbnail]](/uploads/media/thumbnail-280x222-servicenow-and-ai.webp)

![Data Analytics and AI Use Cases in Finance [Thumbnail]](/uploads/media/thumbnail-280x222-combining-data-analytics-and-ai-in-finance-benefits-and-use-cases.webp)

![AI in Telecom [Thumbnail]](/uploads/media/thumbnail-280x222-ai-in-telecom-network-optimization.webp)