Mobile Banking Trends 2020: Streamlined KYC and Digital Account Opening

A Signicat 2019 survey says that over half (56%) of UK retail banking consumers abandoned their online account application processes last year. That’s 35% more than in 2018. What this data is telling us is this: customers’ interest in online banking services and products is growing, but most financial institutions still need to catch up on the latest trends in mobile banking UX.

In this second installment of our Mobile Banking Trends series, we’d like to zoom in on the mobile Know Your Customer (KYC) and digital account opening processes – the core pillars of top-notch mobile banking solutions.

5 Mobile Banking KYC and Onboarding Best Practices

According to CSI, digital onboarding is the second most important technological prerogative for banks in 2020, right after launching a mobile banking app. Indeed, digital remote customer onboarding is key to enabling a smooth digital sales experience and lowering customer acquisition costs (CAC) at the same time. American Banker says that a new digital customer costs banks just $77 to acquire versus $138 for non-digital customers.

What’s standing in the way of those lower CAC costs and higher digital sales for most banks is a rigid know your customer policy. Granted, with the new technological solutions available, it’s possible to maintain absolute levels of know your customer compliance and provide a delightful digital account opening experience at the same time. Below are the best key practices for that.

1. Switch to Simplified Due Diligence (SDD) for Basic Account Opening

Simplified due diligence (SDD) framework, already adopted by the European Banking Authority and equally supported by FATF, legally allows financial institutions to liberalize CDD (customer due diligence) requirements for low-risk activities such as opening a current account or ordering a debit card. Despite having been around for almost 3 years now, these know your customer regulations are mainly used by the digital-only banks and the so-called financial super apps.

In essence, the SDD framework allows you to initially simplify the KYC process for new customers and, thus, create a simple digital account opening process.

SDD Measure

Digital Account Opening Step

You can verify the customer identity either when they apply to open an account or once their transaction volume exceeds a defined threshold.

Collect only basic customer data to speed up the process of opening a new account. Instantly provide the new customer with their account details to start building a usage habit early on.

SDD also allows more means for verifying the customer’s identity based on the:

- Information obtained from one reliable, credible, and independent document or data source only;

- Accepting information obtained directly from the customer when verifying the beneficial owner’s identity;

- Using the source of funds to meet the basic CDD requirements.

Leverage the smartphone’s native functionality such as the camera to enable the customers to submit photos/scans of their ID document, proof of address, etc.

Alternatively, you can integrate that data from another institution such as another bank or FinTech service that the customer used to showcase their source of funds.

In addition, you can use alternative data to verify customer identity and perform basic AML-checks such as location data, customer’s social media digital identities, mobile wallet transactions, etc.

Additional CDD can be applied only when certain events happen – the customer wants to apply for another financial product or has reached a certain transaction threshold.

Impose additional KYC procedures only when the need arises. Before requesting the customer to upload additional information, make sure you’ve tapped into other data sources at your disposal.

As GSMA reports, over 60 countries now have exemptions or simplifications to CDD for certain financial products. In most countries, these provisions will be spelled out explicitly in know your customer laws and regulations. So be sure to check these when creating a working framework for your digital account opening process.

2. Implement Tiered Know Your Customer Rules and Procedures

Tiered KYC is the second step in simplified due diligence. This paradigm stipulates that the more know your customer requirements are met, the greater functionality is delivered to the customer.

For instance, to apply for lending or trading products, you may ask the customer to provide additional insights into their income and occupation. In fact, with the help of machine learning and big data analytics, your bank can develop a custom backend compliance engine that would send alerts and trigger respective compliance steps based on the customers’ data such as:

- Country of residence and local regulations

- Source(s) of income

- Occupation

- Spending and topping-up patterns

- Overall transaction volumes

- Other behavioral patterns

Just how much of an impact can tiered KYC have? GSMA estimates that within two years after introducing this scheme, Mexico has seen a 14% increase in account opening, equal to over 9.1 million new bank accounts. Clearly, that’s a significant portion of previously unharnessed revenues.

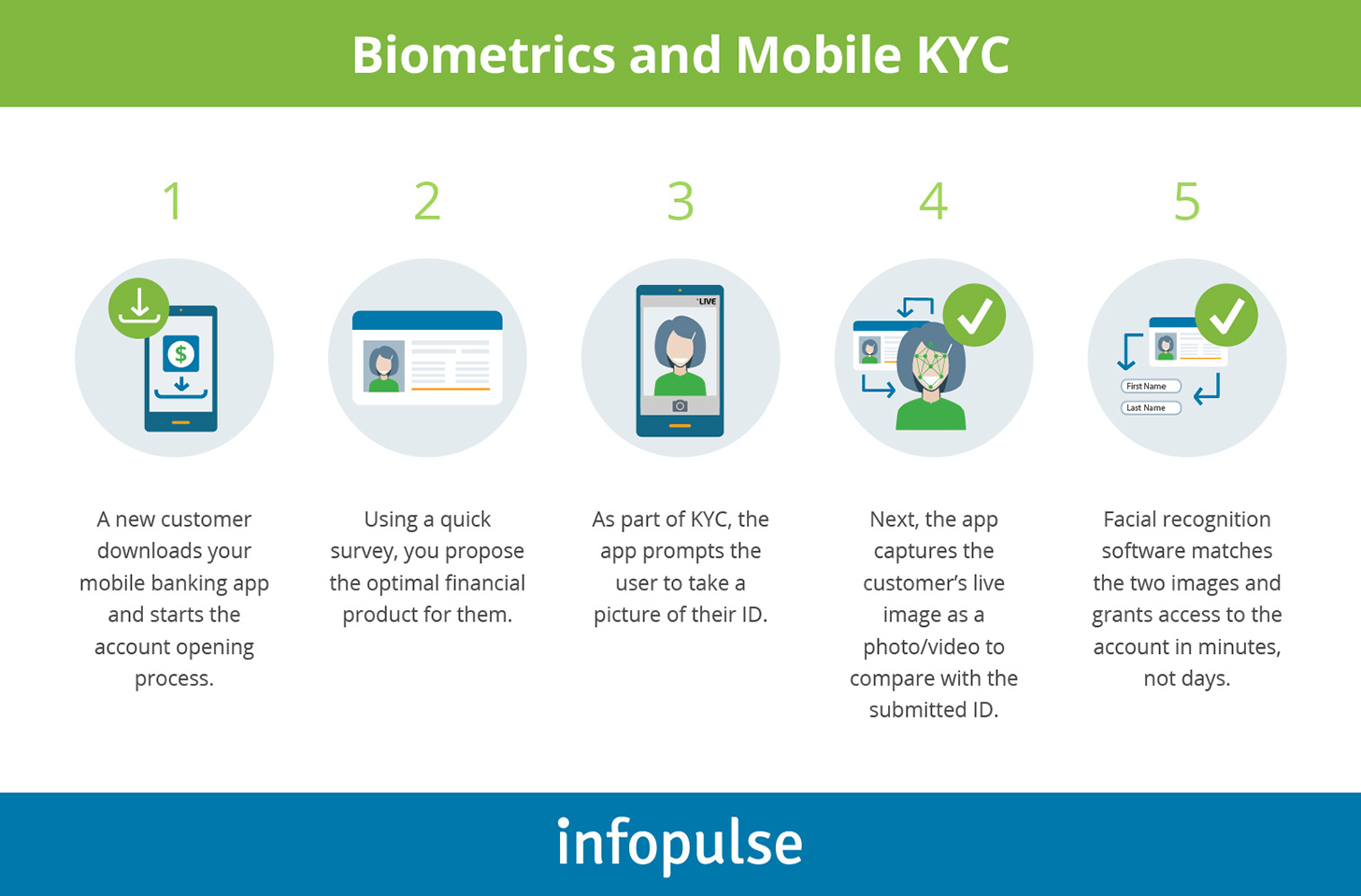

3. Leverage Biometrics to Further Improve UX

The aforementioned Sigma study also points out that 57% of consumers want to (or already use) biometric data to prove their identity. Banks should full-heartedly support this mobile banking industry trend in KYC, as biometrics offers:

- Rapid and highly accurate way of ID verification

- Better security and lower risks of identity theft/forgery

- Seamless authentication for transactions

- Greater convenience, especially on mobile devices

Here’s how a biometrics-powered digital onboarding process can look:

4. Use the Customers’ Multiple Digital Identities for Faster KYC

Rather than asking the customer to provide sensitive personal information over and over again, request access to their credentials from trusted-third parties. Governments worldwide are actively investing in national Digital ID and Mobile ID systems that could be leveraged for KYC.

In the Nordic region, banks, in particular, were the major catalysts for growing usage and acceptance of federated e-IDs. Today, over 70% of citizens in Sweden, Norway, Finland, and Denmark hold a digital identity that they also use for banking services.

Another report from Signicat perfectly sums up all the benefits banks managed to achieve with increased usage of digital identities and digital security mechanisms:

- One bank reports that 8 out of 10 consumer loan applicants completed their applications when using BankID, as opposed to 5 out of 10 prior to its introduction.

- Another Norwegian financial institution reported that e-IDs allowed them to reduce the time for an average mortgage application from 16 days, 70 sheets of paper, and 9 mail dispatches to a 1 day when done digitally. The operational cost savings were significant too.

- If all Norwegian banks adopted digital signatures, the sector could save an estimated 150 million euros annually.

However, to align with existing know your customer banking regulations, most banks will need to ramp up the security of issued digital identities.

5. Reduce Risks with Machine Learning and Predictive Analytics

Every know your customer checklist places a great emphasis on anti-money laundering and minimization of other financial fraud. That’s part of the reason why many banks don’t feel confident enough to simplify CDD or retire certain KYC procedures.

However, as speed and convenience in financial services provisioning have become key differentiating factors for consumers, holding on to outdated policies presents more risks than relaxing the requirements. Especially, when these relaxations are backed by state-of-the-art anti-fraud analytics systems that progressively learn over time to become even more accurate.

Asian FinTechs are leading the way when it comes to fast, effective, and secure ML-driven customer background checks.

For instance, KakaoBank, the first digital-only bank in South Korea, managed to onboard over 1 million customers within 5 days after launch – all thanks to streamlined KYC and back-office operations powered by AI and Machine Learning. With an intelligent credit-scoring algorithm, the neo-bank also became the largest loan issuer in the domestic market, running ahead of 19 more established, incumbent banks with approx. $3.6 billion worth of deposits accepted and over $3 billion loans issued.

Banks in other markets can certainly take the cue from their Asian counterparts and look more into ML-powered fraud detection systems and AML-solutions.

To Conclude

It’s a fact: consumers demand better remote digital onboarding experience. Banks that manage to deliver it, leave even more established competitors well-behind in terms of account opening rates. Few customers will now settle for extended, paper-based application forms or multiple visits to the branch. As the online and mobile banking trends grow stronger on a global scale, building a better digital account opening system and upgrading the KYC process is a strategic necessity for banks.

Stay tuned for the next installment in our mobile banking technology trends series, covering another integral aspect of KYC and customer account security – biometrics!

And in the meantime, reach out to Infopulse financial team to discuss the scope of possible improvements for your digital banking products!

![CX with Virtual Assistants in Telecom [thumbnail]](/uploads/media/280x222-how-to-improve-cx-in-telecom-with-virtual-assistants.webp)

![Generative AI and Power BI [thumbnail]](/uploads/media/thumbnail-280x222-generative-AI-and-Power-BI-a-powerful.webp)

![AI for Risk Assessment in Insurance [thumbnail]](/uploads/media/aI-enabled-risk-assessment_280x222.webp)

![Super Apps Review [thumbnail]](/uploads/media/thumbnail-280x222-introducing-Super-App-a-Better-Approach-to-All-in-One-Experience.webp)

![IoT Energy Management Solutions [thumbnail]](/uploads/media/thumbnail-280x222-iot-energy-management-benefits-use-сases-and-сhallenges.webp)

![5G Network Holes [Thumbnail]](/uploads/media/280x222-how-to-detect-and-predict-5g-network-coverage-holes.webp)

![How to Reduce Churn in Telecom [thumbnail]](/uploads/media/thumbnail-280x222-how-to-reduce-churn-in-telecom-6-practical-strategies-for-telco-managers.webp)

![Automated Machine Data Collection for Manufacturing [Thumbnail]](/uploads/media/thumbnail-280x222-how-to-set-up-automated-machine-data-collection-for-manufacturing.webp)

![Money20/20 Key Points [thumbnail]](/uploads/media/thumbnail-280x222-humanizing-the-fintech-industry-money-20-20-takeaways.webp)