Blockchain in Non-Financial Industries: Overview

Pic 1. Blockchain as High Interest of Market.

Blockchain Potential

The blockchain is a distributed database technology that was swiped from the Bitcoin when it turned out that it has a bigger potential to manage not only cryptocurrencies, but also exchange of other different values. The main advantage of the blockchain is that it allows synchronization of the unlimited databases that belong to the network participants who don’t trust each other. Using the state-of-the-art cryptography and distributed ledger – a dynamic, digital database held and updated independently by each participant (node) that does not require a central authority for data reconciliation – the system becomes a perfect solution to build decentralized environments for independent parties who want to cooperate within a short time based on the consensus principles.

Elimination of intermediaries is a key blockchain’s feature and a game-changing opportunity for our world. Without third parties involvement, users become in control of all their operations and values shared. As each party is interested in the verity of the information and responsible for transactions’ validation, the risk of dirty deals is extremely low.

The particular appeal of the blockchain, in this case, is derived from the “smart contract” – the new computer protocol, which digitally facilitates, verifies and/or enforces the performance of a certain agreement. Blockchain-based smart contracts impartially regulate all users’ activities without the middleman participation leaving users ahead of their information and processes. While the script language provided by Bitcoin allows creating only a limited set of custom contracts to support escrows, cross-chain trading or multisignature account, Ethereum has made one step further and enables developers to use a Turing-complete language on its blockchain to create truly custom smart contracts. Instead of the legal lingo, a set of terms and conditions that the other parties agree to abide is written in code and placed on the blockchain. As long as the code is executed as intended, the contract remains secure and impossible to breach.

Smart contracts have allowed reconciling a large array of blockchains existing out there and powering specific applications. Instead of developing new blockchains for a different type of application, smart contracts made it possible to add several types of applications to a single blockchain and make sure that all of them follow the same set of rules. Additionally, smart contracts have enabled users to create niche agreements for small operations – when it doesn’t make sense to create a separate new blockchain to govern those. For instance, a small business owner wants to place an order with a new supplier he does not trust yet. The party can then create a smart contract that will outline the deliverables and associated delivery terms, lock the pre-payment for 10 days and the vendor will get paid once the goods have arrived and if all the specified terms are met.

Within the financial industry, smart contracts are expected to save investment banks up to $12 billion annually as the code could automatically perform intended actions when a predefined condition occurs, thus eliminating the need for manual interference. Deploying smart contracts to govern financial reporting could also cut down the infrastructure costs by 30% on average, while ensuring better transparency and data quality. Finally, the compliance costs and centralized security operations such as “know-your-customer” checks can be reduced by 50%. The very same approach can be used towards optimizing a wide range of transactions happening in other industries, as the paper will further illustrate.

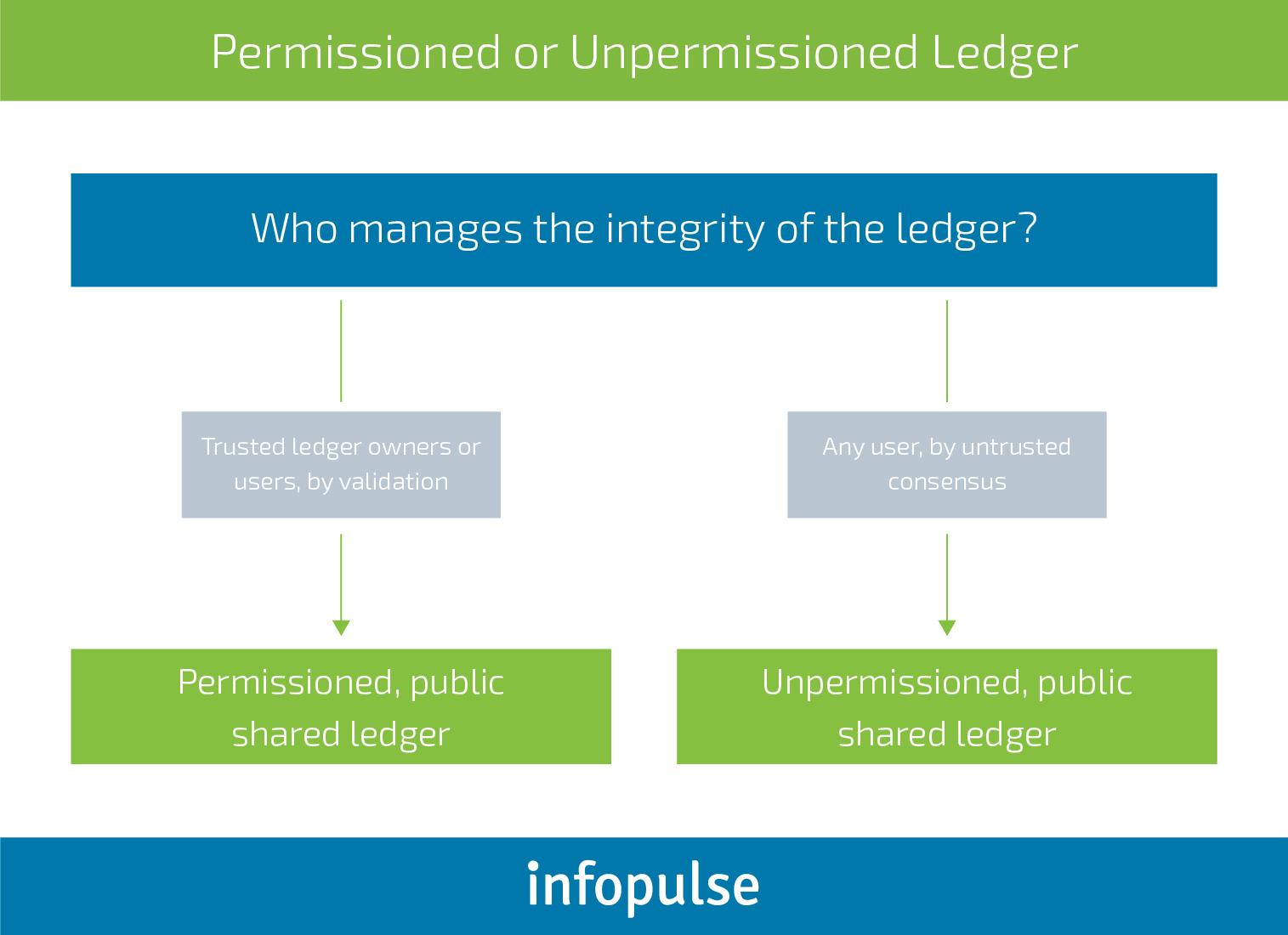

Another strength of the blockchain technology is its separation into public and private approaches with different permissions structures. In general, there are three types of blockchain networks an organization can develop:

1. Public blockchain.

It is the type of chain, any participant can read, add transactions to and expect them to get included as long as they are valid; and participate in the consensus process – that is determine whether a new block should be added to the chain. All the actions on the public blockchain are secured by cryptographic verification mechanisms such as proof-of-work or proof-of-stake. Such chains are usually characterized as “fully decentralized” as there’s no single controlling authority to govern the consensus process.

2. Consortium blockchains.

It is the type of blockchain, where the consensus processes are governed by a selected set of nodes (or entities). For instance, there’s one company with 15 board members, each of whom operates one node. To validate a new block, 10 out 15 members should sign it. Consortium blockchains can have a public or restricted right to be read. Some chains also allow the general public to add only a limited number of queries and add new blocks only to selected parts of the blockchain. Typically, such blockchains are characterized as “partially centralized”.

3. Fully private blockchains.

The write permissions here are centralized to one node. The right to read may be public or restricted to certain participants only. For instance, such chains can be used for internal database management within a single company.

Pic 2. Permissioned or Unpermissioned Ledger.

The access control mechanism for private and consortium blockchains can vary depending on the owners’ needs. Some of the common options here are the following:

- Existing participants can decide on and invite new participants.

- A regulatory body can issue keys/license for participation.

- The governing consortium decides on the future entrants.

Permissioned blockchain technology is a topical subject breaking new ground for the effective and secure data managing. For sure, the Blockchain technology shouldn’t be considered only as an innovative solution for the financial sector. Setting all known transaction systems on their ears, the Blockchain also provides startups with an economic growth and helps to protect and support the development of smart cities. Blockchain has already shown its potential in a wide number of areas. Let’s take a closer look at how it may affect non-financial industries, namely:

- Blockchain in Healthcare.

- Blockchain in Government Services.

- Blockchain in the Energy Industry.

- Blockchain in Insurance.

- Blockchain in Manufacturing.

- Blockchain in Telecom.

1. Blockchain in Healthcare.

Healthcare industry generates terabytes of information every day ranging from patient information to payment data and clinical trial results. Storing, exchanging and protecting this type of data is critical for healthcare providers. However, managing and reconciling the data from multiple sources is challenging.

Blockchain can be used to positively impact the movement of big data between different parties, streamline and secure those transactions; improve billing procedures; contract and asset management workflows; and improve data exchange among different medical devices including IoT.

This technology can successfully tackle the next pressing industry hurdles:

- Fragmented data: blockchain enables decentralized data storage and accumulation using multiple computer networks, thus eliminating the single point of failure.

- Timely Data Access: data stored on the distributed ledger enables real-time updates across all the networks.

- Security: all the transactions are immune to 3rd party hampering. Personalized access keys protect patient identity and prevent unauthorized access.

- System Interoperability: blockchain delivers a universal global system authentication method, enabling data exchange among all types of systems.

- Patient-generated data: information from IoT gadgets can be instantly added to the chain and shared with respective parties.

- Cost-effectiveness: the cost of one transaction can be significantly reduced; elimination of third-party applications (such as cloud services) reduces the time lag in data access.

Read more on the blockchain use cases in healthcare.

2. Blockchain in Government Services.

Progressive governments now strive to build a more transparent and collaborative rapport with the citizens and streamline the routine bureaucratic processes ranging from the registration of assets to voting and government contract management.

Blockchain has become the key tool to support such initiatives as the technology enables seamless and secure data exchange, storage, and registry. Critical information can be shared seamlessly, openly and securely, while remaining accessible to the general public. Most governmental blockchain projects are still in the development stage, yet promise to bring significant shifts within multiple domains:

- Digital identity management: blockchain can deliver unified standards for storing and exchanging citizens’ identity data. The creation of a self-sovereign digital identity, in turn, enables more efficient transactions across various domains including elections, healthcare, and law.

- Recordkeeping: all the records can be stored on a distributed ledger thus eliminating the reliance on a trusted third party. While remaining immutable, those records also become easier to access, manage and audit when needed. Blockchain-based recordkeeping can be used to improve a large array of registration and compliance processes within the government.

- Smart contracts allow governments to enable higher efficiency and streamline the execution of routine transactions; thus ensure the timely and proper delivery of public services.

- Higher visibility for regulatory compliance. Compliance across different domains and industries can be monitored and audited automatically, in real-time. Regulated entities, in turn, can receive timely notifications about the changes in compliance and act accordingly within the shortest time frame. Fraudulent activities or breaches would be easier to detect and investigate.

Read more on the blockchain use cases in the government sector.

3. Blockchain in the Energy Industry.

The rising adoption of IoT gadgets powering the smart city ecosystems, electric vehicles and virtual plants poses new challenges for the energy market. As the global demand for power keeps rising, key players will need to perfect their balancing act and optimize the supply process.

The rise of the so-called prosumer – an active class of consumers generating and accumulating their own energy – also agitates the energy market to become less centralized and more accessible to individual entrants.

Peer-to-peer electricity trading projects have been tested in multiple locales around the globe with the help of blockchain. The technology enables higher visibility and allows to trace and audit all the energy exchange transactions happening between different entities. The technological nature of blockchain also promotes higher trust and reduces the need for a centralized authority or intermediaries during the power exchange process.

Beyond P2P energy trading, blockchain technology can drive value for the following processes:

- Virtual Power Plants Management and Performance Optimization. VPPs performance can be largely enhanced with the help of blockchain as the technology enables to automatically match the produced resources with the demand response programs; wholesale them through smart contracts, and adjust the VPPs performance depending on the current market conditions.

- Grid security. KSI (Keyless Signature Infrastructure) blockchain-based technology can be used to create a data exchange ecosystem between all the “smart devices” on one grid and reduce the chances of any external hampering.

- Unified storage of all transactional activities. Recordkeeping on the blockchain is tamper-proof and easy-to-audit. Regulatory authorities will have more visibility into all the operations including emission allowances and renewable power certificate management.

Read more on the blockchain use cases in the energy sector.

4. Blockchain in Insurance.

Insurance contains two types of data: static – all information records, and dynamic – transactions that should be managed by both insurance vendors and consumers. Moreover, the main requirement for this data is that it has to be available on the knocker. Such conditions impose creation of the strong and secure system that could manage all this data in a proper way. Fortunately, we already have such system – the blockchain.

Implementing the blockchain in insurance will help to enhance and simplify all related processes, namely, records maintaining, contracts signing, claims registration and assessment, payment and closure. Ultimately, blockchain can cut costs, improve customer service and manage risks for insurance companies.

The most transformative use cases of blockchain in the insurance industry include the following ones:

- Streamlined claims management. A single claim may have to go through multiple checkpoints to verify its validity and avoid potential fraud. The blockchain technology can help reduce the duplicate and unnecessary verification processes; decrease the administrative costs and ensure seamless contract handling between all parties involved.

- Proof of Insurance can become an easy-to-review digital asset with the help of blockchain, eliminating the associated paperwork.

- Management of multinational policies can take place on a distributed ledger. Different policies can be coded as a “smart contract”, meaning that the applications will automatically verify cross-compliance; reconcile and exchange information on policies updates in real-time.

- KYC/AML Implementation with blockchain eliminates the need for multiple checkups; speed up the verification processes and exclude the possibility of fraud.

- Contract Lifecycle when facilitated on blockchain eliminates the chance of errors, fraud or data inconsistency. Furthermore, it can help ensure timely and secure access to the newest updates; make the exchanged information more transparent and accessible.

Read more on the blockchain use cases in the insurance sector.

5. Blockchain in Manufacturing.

While most blockchain research endeavors are concentrated around financial applications or the technology itself, the interest to use blockchain in the manufacturing industry is gaining momentum. Current studies foresee that in some 20 years the blockchain will dramatically change the face of modern manufacturing. This transition is called the fourth industrial revolution (Industry 4.0).

Blockchain applications in manufacturing industry have presently shaped into three main usage areas:

- Supply chain management/auditing, and digital product memory. Due to its inherent transaction transparency, blockchain can be used to make any deliveries traceable in terms of product origin, quality, certifications, movement, transaction history, and all other relevant product information throughout the entire supply chain. A good example is IBM and Maersk to implement blockchain for tracking containers during the shipping process, or Everledger to register certifications and transaction history of diamonds. Moreover, engagement of smart contracts can drastically reduce paperwork, cost and time spent on execution of supply contracts.

- Industry 4.0 and Internet of Things (IoT). In this area, blockchain can resolve the identification issues of IoT devices simultaneously reducing the vulnerabilities related to this process. A digital identity built on blockchain cannot be compromised while the device ID data can be dynamically updated. In Industry 4.0, blockchain allows timestamping of sensor information to prevent any further data manipulation and make sure that all required standards are met, which increases trust between the parties.

- 3D printing. Applying blockchain in the 3D printing reduces supply chain overhead costs. For example, a design project is uploaded to the blockchain and automatically encrypted, thus protecting it from plagiarism. Then the blockchain smart contracts tied with the project file look up the nearest 3D printers, logistic service providers, etc., negotiate the best price and conditions, and initialize execution eliminating third parties in the supply chain. When the project is 3D-printed, the blockchain labels it with a digital product memory, which includes full project history like materials used or the ownership details. This information not only deepens trust between the parties, but also serves as a basis for warranting, maintenance or recycling purposes.

Read more on the blockchain use cases in the manufacturing industry.

6. Blockchain in Telecom.

Until recently, the telecom sector has kept afar from the blockchain scene just watching with mere curiosity the “fancy” technology spreading in other industries. Now telecom’s growing interest to “distributed ledgers” (a general nickname for different kinds of blockchains) is obvious.

Besides common expectations like reducing costs and improving efficiency of existing processes and infrastructure, Communication Service Providers (CSP) see the blockchain technologies to evolve in the following areas:

- 5G: new mobile standards. 5G technology is currently in development, but soon will revolutionize the way we use telecommunication services. It will provide bigger speeds of connection – up to 1,000x faster than 4G, potentially exceeding 10Gbps. This technology can operate without blockchain, but its implementation will make it easier and cheaper for both service providers and their customers.

- Fraud prevention – new standards of digital security. Blockchain is protected from fraud by nature. Its architecture combines transparency and security at the same time – features that usually stand by the opposite ends of the scale. Blockchain encrypts all received information into hash-code made available for all to see. Thus, any transaction becomes transparent, though you can see it only in encrypted form as a string of random letters and numbers. Given that data is transferred at a high speed, it is impossible for a hacker to decrypt it in flight. Besides, there is no way to erase or compromise data in the blockchain due to its storage and exchange operations are distributed between a huge number of nodes. Telecom companies can use blockchain technology as a platform for all their processes bringing information security and data protection to a new level.

- Identity-as-a-service: secure digital identity stored on blockchain. Identity-as-a-service is the third application area, where telecom providers can find great opportunities to improve and find new revenue sources. Proving one’s identity and credentials traditionally went through signing physical or digital documents. That requires involving third parties to confirm identity, to process personal data, etc. which raises a trust issue. There is no guarantee that third parties are totally reliable, that the services one signed up for will be received, and that customer’s personal information will not be stolen or compromised. Blockchain resolves trust issues easy by creating 100%-proof digital identity based on public/private key pair encryption.

Read more on the blockchain use cases in the telecom sector.

To sum it up, blockchain implementations in the non-financial sector can provide advancements never seen before. New ideas of blockchain realizations arise every day. However, despite the massive hype around blockchain as a universal solution and a new hi-tech religion, it is worthwhile to have a look at the other side of the matter.

In the next article, we will explore the pros and cons of blockchain era with regard to non-financial industries.

![CX with Virtual Assistants in Telecom [thumbnail]](/uploads/media/280x222-how-to-improve-cx-in-telecom-with-virtual-assistants.webp)

![Generative AI and Power BI [thumbnail]](/uploads/media/thumbnail-280x222-generative-AI-and-Power-BI-a-powerful.webp)

![AI for Risk Assessment in Insurance [thumbnail]](/uploads/media/aI-enabled-risk-assessment_280x222.webp)

![Super Apps Review [thumbnail]](/uploads/media/thumbnail-280x222-introducing-Super-App-a-Better-Approach-to-All-in-One-Experience.webp)

![IoT Energy Management Solutions [thumbnail]](/uploads/media/thumbnail-280x222-iot-energy-management-benefits-use-сases-and-сhallenges.webp)

![5G Network Holes [Thumbnail]](/uploads/media/280x222-how-to-detect-and-predict-5g-network-coverage-holes.webp)

![How to Reduce Churn in Telecom [thumbnail]](/uploads/media/thumbnail-280x222-how-to-reduce-churn-in-telecom-6-practical-strategies-for-telco-managers.webp)

![Automated Machine Data Collection for Manufacturing [Thumbnail]](/uploads/media/thumbnail-280x222-how-to-set-up-automated-machine-data-collection-for-manufacturing.webp)

![Money20/20 Key Points [thumbnail]](/uploads/media/thumbnail-280x222-humanizing-the-fintech-industry-money-20-20-takeaways.webp)