![Overview of Connected Banking and its Benefits [banner]](https://www.infopulse.com/uploads/media/what-is-connected-banking-its-promises-and-benefits-1920x528.webp)

What Is Connected Banking: Its Promises and Benefits

Why Do We Need Connected Banking?

First things first, connected banking is a digital ecosystem of front-office and back-office systems combined with new technology standards and risk management requirements.

To get a better understanding of how it looks in practice, you can read our detailed case study for one of the top 20 world banks. In this project, we have produced a complex wholesale management system for the risk management department of the bank.

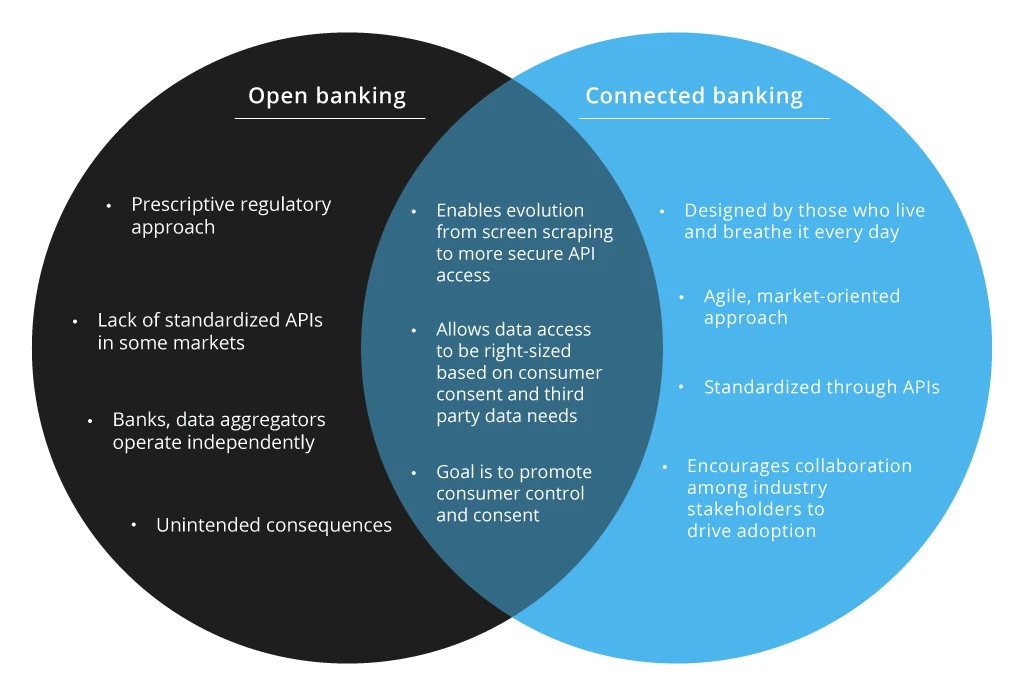

How is connected banking different from open banking then, you ask?

While open finance business model allows for faster and more convenient services, the matter of data security and transparency still needs to be solved – banks control and grant access to customers’ data. That’s what connected banking is set to resolve with a new approach to data privacy that puts a customer in charge of sharing their own sensitive information. Because all the players in this financial ecosystem work under different rules and regulations, cohesively integrating them under one tech framework calls for heavy lifting across all fronts. Legacy banking systems modernization is the first logical step that financial institutions can take in this process.

The challenge lies in customers’ sensitive data that gets shared back and forth between banks, data aggregators, and third parties. Financial apps store bank account and login information that can cause serious harm to all parties in the case of a data breach. On top of that, customers usually don’t have a clue about what types of their data are stored and shared. According to KPMG corporate data responsibility survey, 49% of end-users reported that they don’t know how to protect their data, with 64% of companies admitting that they don’t address this problem.

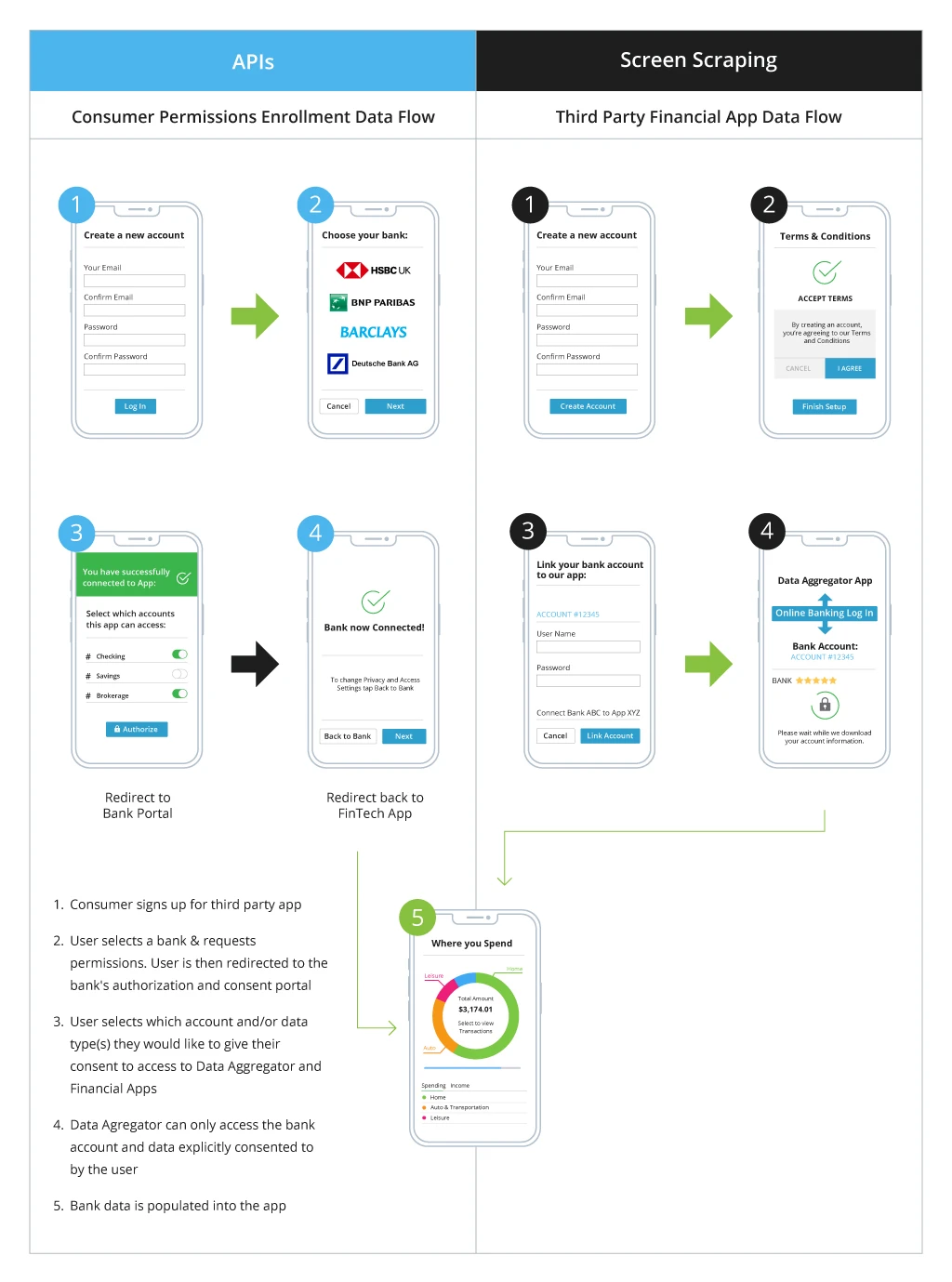

In 2019, the European Commission attempted to strengthen the security of customer data by adding a new law to the PSD2 directive that would ban the use of screen scraping. Screen scraping allows third parties to access one’s bank account with their login details ‘as if they were you’. In contrast, an Application Programming Interface (API) method grants data access without the need to share one’s account credentials. That’s why API acts as one of the central pillars of connected banking and a key technology for protecting critical financial information.

Essential Characteristics of Connected Banking

1. API standards

As we have already mentioned, API standards are a crucial tech component of the connected banking paradigm. APIs are a perfect tool for customer data control thanks to the tokens that include consumer preferences regarding the data points stored and shared between banks and third parties.

Why is this so important? For starters, commerce has almost entirely moved online. Barclays revealed that in 2020, 88.6% of transactions were contactless. And if we dig deeper, we see that the percentage of people using online banking channels in the eurozone increased to 61% in 2022.

Nowadays, we receive financial services not only from traditional banks but also from various industry disruptors like FinTechs with their non-stop innovations and Meta, Apple, and Google tech giants. With loose entry rules, open finance virtually eliminated the boundaries between tech and finance. Anyone who can deliver a superb banking experience and provide sought-after customer intimacy wins the most valuable asset – a loyal customer.

2. Standardization principle

To compete with the hard-to-resist financial inclusion of FinTechs, peer-to-peer lending, trading platforms, cryptocurrencies, or even ride-sharing apps offering loans, traditional banking institutions need to become an essential part of the new hyper-connected financial ecosystem. A global attempt and a market-based approach to standardizing technology, vendor processes, and consumer privacy are needed to make it possible, making this standardization principle another key characteristic of connected banking.

3. Centralized network infrastructure

Finally, without a centralized network infrastructure, it’s a bit cumbersome to meet the modern needs of customers. They want to benefit from a third-party savings app that would aggregate information from all their banking accounts but, at the same time, make them feel confident that their data is safe and private. Of course, banks have been slowly establishing integration relationships with various digital natives. But the industry needs a more centralized approach to management and compliance to make these alliances secure, scalable, and future-proof.

Speaking of future-proof, penetration testing against information security risks is a basic housekeeping practice that most financial institutions often overlook. Check this case for ING Bank Ukraine, where you can find more details on why security evaluation is so critical.

What Benefits Connected Banking Has to Offer?

Fewer people choose to go to a banking branch to open an account, apply for a loan offline, and decide for themselves which of the countless deals will bring them the most value. Modern customers love to do their banking digitally, on-the-go, and through a channel of their choice (thank you, omnichannel banking for that).

But there is still friction when it comes to synchronizing the smooth running of all the processes and ensuring 100% data security and privacy. Connected banking literally fills in these gaps and adds a list of benefits for all the involved parties (partners, customers, and all stakeholders):

- Streamlined customer experience with fast and intuitive services

- Extended security practices

- Customers are in control over their own shared sensitive data

- Access to a broader range of products/services from a single access point

- Amplified operational efficiency with hyperautomation

- Accurate governance, risk, and compliance management

- Single transaction interface for all banking and accounting services

In Conclusion

So, in the consumer-first age, confusing privacy terms, the slightest chance of cybersecurity threat, and limited functionality are the looming deal-breakers. Connected banking aims to tackle these challenges by connecting clients, systems, and features of financial institutions and third-party providers.

How? Through automation and advanced digital solutions that lay the foundation of the flexible and hyper-connected financial ecosystem of the near future.

![CX with Virtual Assistants in Telecom [thumbnail]](/uploads/media/280x222-how-to-improve-cx-in-telecom-with-virtual-assistants.webp)

![How to Build Enterprise Software Systems [thumbnail]](/uploads/media/thumbnail-280x222-how-to-build-enterprise-software-systems.webp)

![Super Apps Review [thumbnail]](/uploads/media/thumbnail-280x222-introducing-Super-App-a-Better-Approach-to-All-in-One-Experience.webp)

![IoT Energy Management Solutions [thumbnail]](/uploads/media/thumbnail-280x222-iot-energy-management-benefits-use-сases-and-сhallenges.webp)

![5G Network Holes [Thumbnail]](/uploads/media/280x222-how-to-detect-and-predict-5g-network-coverage-holes.webp)

![How to Reduce Churn in Telecom [thumbnail]](/uploads/media/thumbnail-280x222-how-to-reduce-churn-in-telecom-6-practical-strategies-for-telco-managers.webp)

![White-label Mobile Banking App [Thumbnail]](/uploads/media/thumbnail-280x222-white-label-mobile-banking-application.webp)

![Money20/20 Key Points [thumbnail]](/uploads/media/thumbnail-280x222-humanizing-the-fintech-industry-money-20-20-takeaways.webp)

![Deepfake Detection [Thumbnail]](/uploads/media/thumbnail-280x222-what-is-deepfake-detection-in-banking-and-its-role-in-anti-money-laundering.webp)