From Neobanks to Neobrokers: How to Take the Next Step in Digital Banking Evolution

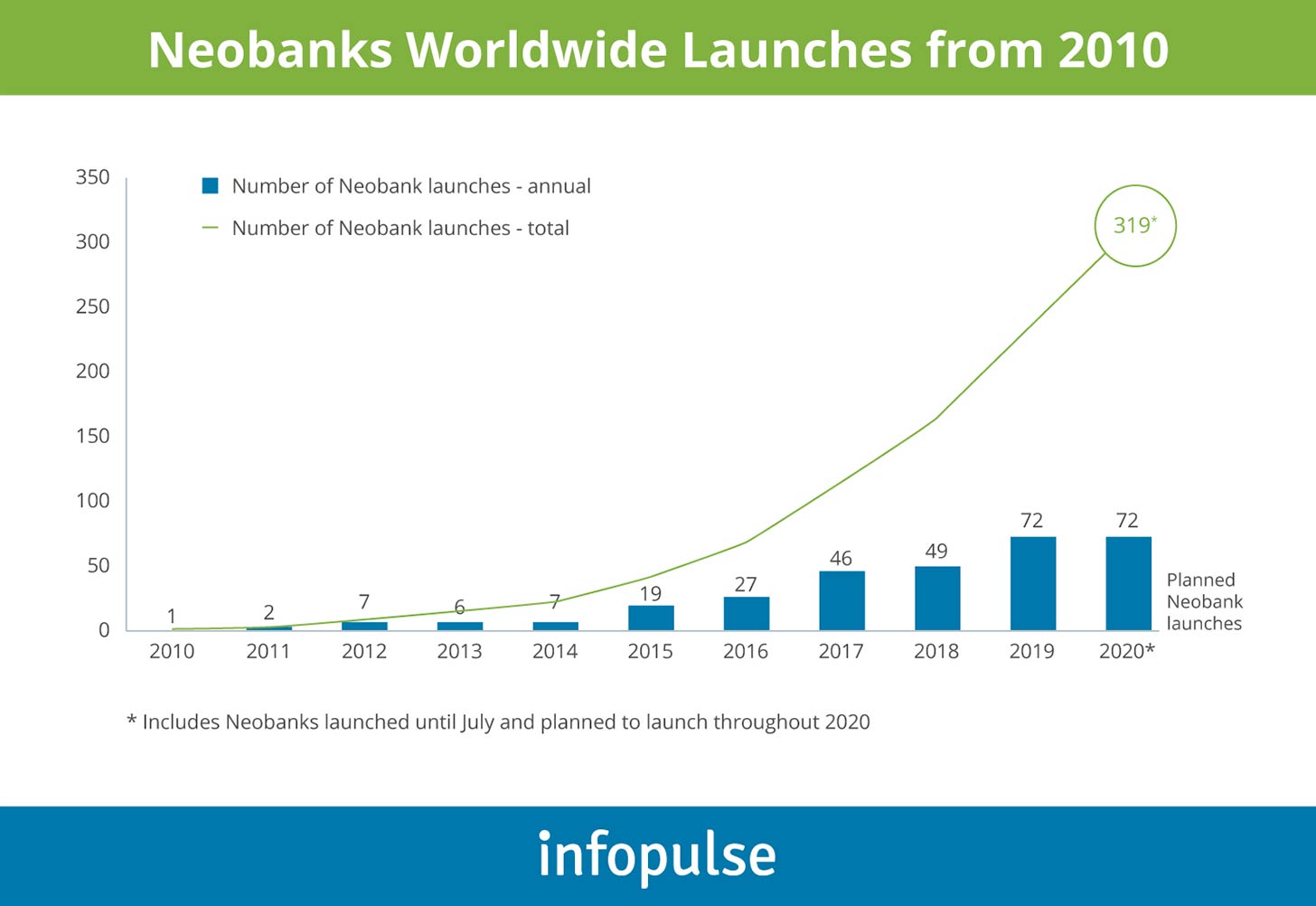

Agile, digitally-first, and capable of rapid product development via public APIs, neobanks have rapidly penetrated the retail banking market and have already taken over some of the most profitable verticals such as payments and remittances, lending, and more recently — wealth management.

Revolut allows customers to invest in crypto currencies and asset tokens (Gold). Swissquote’s customers can open a private trading account online to access an array of trading tools — from traditional stocks to forex and crypto-assets, as well as benefit from robo-advisory services. Monzo provides customers an ability to sign up for a selection of savings plans with different interest rates, enabled by partnering financial institutions. Step by step, digital banking is embracing wealth management as one of its essential features.

Why Wealth Management Services are the Next Frontier for Neobanks

Despite (or rather due to) rapid pursuit of growth across multiple vectors — customer acquisition, market penetration, customer retention — even unicorn neobanks are struggling to consistently make a profit. British neobank Starling broke even for the first time only in October 2020 (after launching in 2014) when it reached over 1.8 million accounts and £4 billion in deposits.

As consumer spending went down in 2020 due to the pandemic, mobile digital banks have found themselves in a tricky position: they were not earning the traditional account fees (unlike incumbents) as most offer no-fee accounts. The profit margins from card transactions alone could not sustain them either. Respectively, some players actively sought revenue stream diversification through complementary offerings — insurance, trading, and most recently wealth management products.

Traditionally, private wealth management was a service the selected few could afford or felt necessary to obtain. Digitization of the banking sector has lowered the entry-barrier for obtaining focused wealth management, delivered by the algorithms rather than human advisors.

Increasingly, consumers are on board with such service models. Over 72% of high-net-worth individuals (HNW) aged below 40 feel comfortable working with a virtual financial advisor. What is even more interesting is that ultra-high-net-worth (UHNW) individuals seek out digital wealth management providers specifically. According to EY Global Wealth Management Report, 45% of wealth management clients plan to use a fintech provider in the next 3 years (or less).

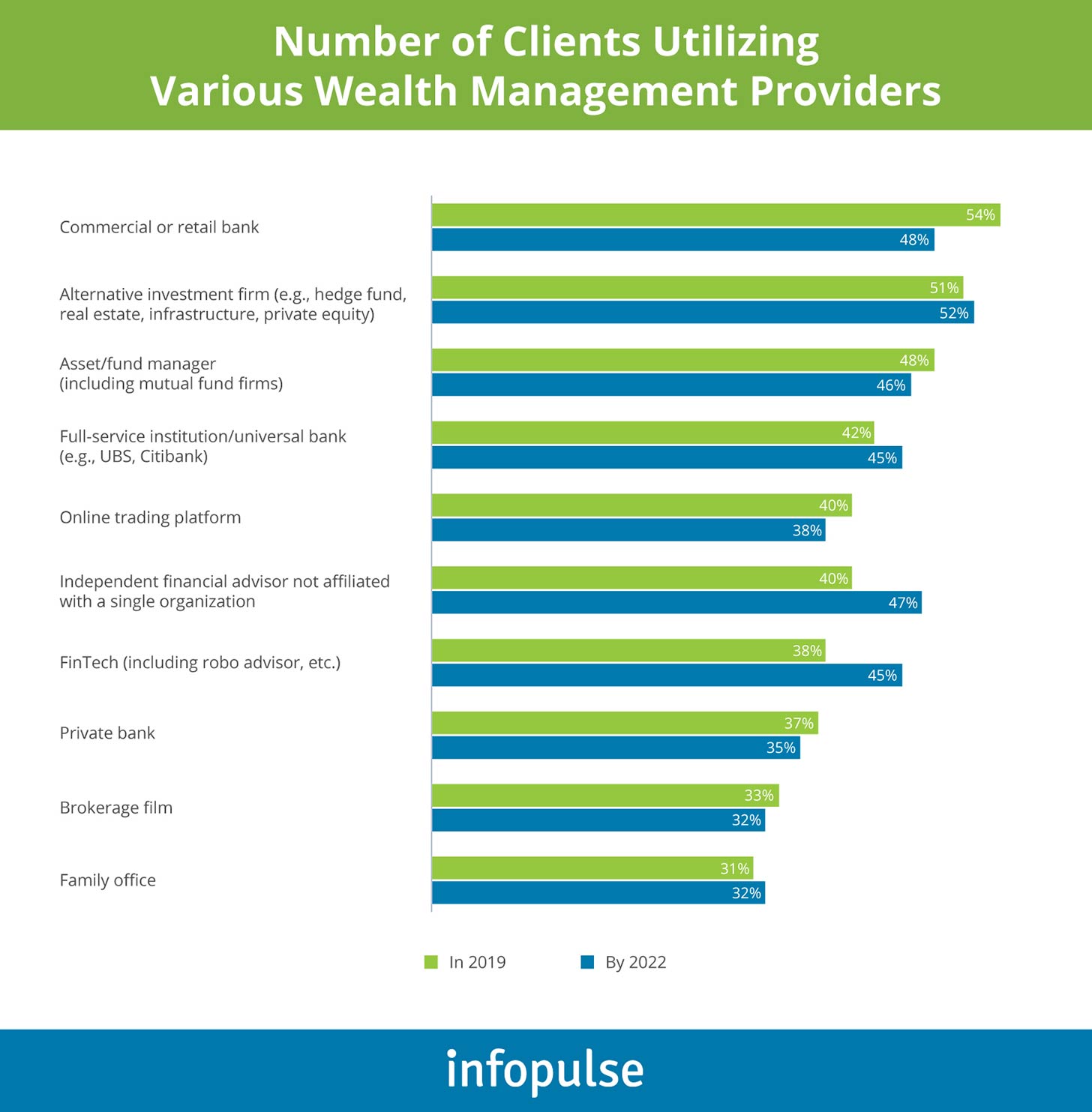

While the majority of clients change wealth management providers due to a major life event (marriage, divorce, new job, etc), pricing and service levels are also detrimental to their decision for staying with a provider.

Capgemini reports that HNWs are growing less comfortable with wealth managers’ fees — 33% were unsatisfied in 2019. In fact, “high fees” are cited as the top reason for considering the change of providers by 42% of HNWs. Additionally, 60% of respondents also reported poor experience during their attempts to gain more information about new offerings.

Given the above, it makes sense why as much as 74% of HNWs are willing to consider wealth management software from BigTech firms. Even more interesting is the fact that among clients who are planning to switch in the next 12 months, 94% would consider offerings from BigTech firms.

What this data is telling us is this: incumbents are far from excelling in digital CX. It follows that their clients are growing less satisfied with the cost and quality of the provided services. Traditional banks have a limited purview into customer churn and oftentimes fail to prevent attrition. Given the audience’s growing interest in fintech offerings, neobanks are well-positioned to attract a flux of HNWs customers since digital wealth management is profitable, and yet unharnessed turf.

How Neobanks Can Transition To Become Neobrokers

Wealth management clients are growing distressed with the digital service levels that traditional players provide for the price they demand. Their positive experience with other fintech products also makes them more inclined to consider a digital wealth management solution. Such a “vote of confidence” provides neobanks with some headroom for customer acquisition. Especially, if they focus on the following activities.

Capitalize on Current Strengths and Data Capabilities

BCG states that global wealth management leaders will be determined by the ability to obtain client-specific insights and act on them rapidly. In other words, personalization and a strong alignment between the product portfolio and customers’ needs will be integral for leading in the digital space.

Neobanks already have a good picture of their customers’ finances and spending habits. Especially, if they also provide bank account aggregation capabilities and let users connect accounts from other financial service providers. Using this data, neobanks can develop new personalized products and offerings, catering to the different steps of the customers’ journey.

In fact, that’s what SoFi did back in the day. A mobile-first personal finance company, now valued at $9 billion, was originally launched as a debt refinancing and lending comparison tool. By continuously collecting and operationalizing customer data and feedback, SoFi worked out a set of complementary financial offerings — lending, investment, insurance, wealth management, banking — and morphed into a comprehensive financial platform, serving a wide spectrum of customers’ needs.

The takeaway: capitalize on customers’ data (generated and aggregated from connected services) to guide your product development decisions.

Provide Personalized Portfolio Construction and Advisory

A simple fact that drives the growth of “Robo” and AI-powered investing solutions is the fact that personal finances appear to be too complex and boring for most consumers. A Credit Karma survey notes that 46% of their consumers find finances overwhelming. At the same time, a far lower percentage can afford a private personal financial advisor.

The commoditization of ML and AI technologies in finance made it possible to deliver personalized financial advisory services at scale for an affordable price.

Robo wealth management platforms already simplified access to tailored advice and financial guidance. Since they already have fuller information about the customers’ money movements, neobanks can take this a step further and delight users with integrated wealth management capabilities such as:

- Provide personalized portfolio allocation tips

- Suggest new asset recommendations based on tolerated risks

- Allow modeling different investment scenarios to meet the set financial goals

- Engage in day-to-day personal finance coaching

- Connect with human financial advisors for more complex questions.

Focus on Underserved Asset Segments

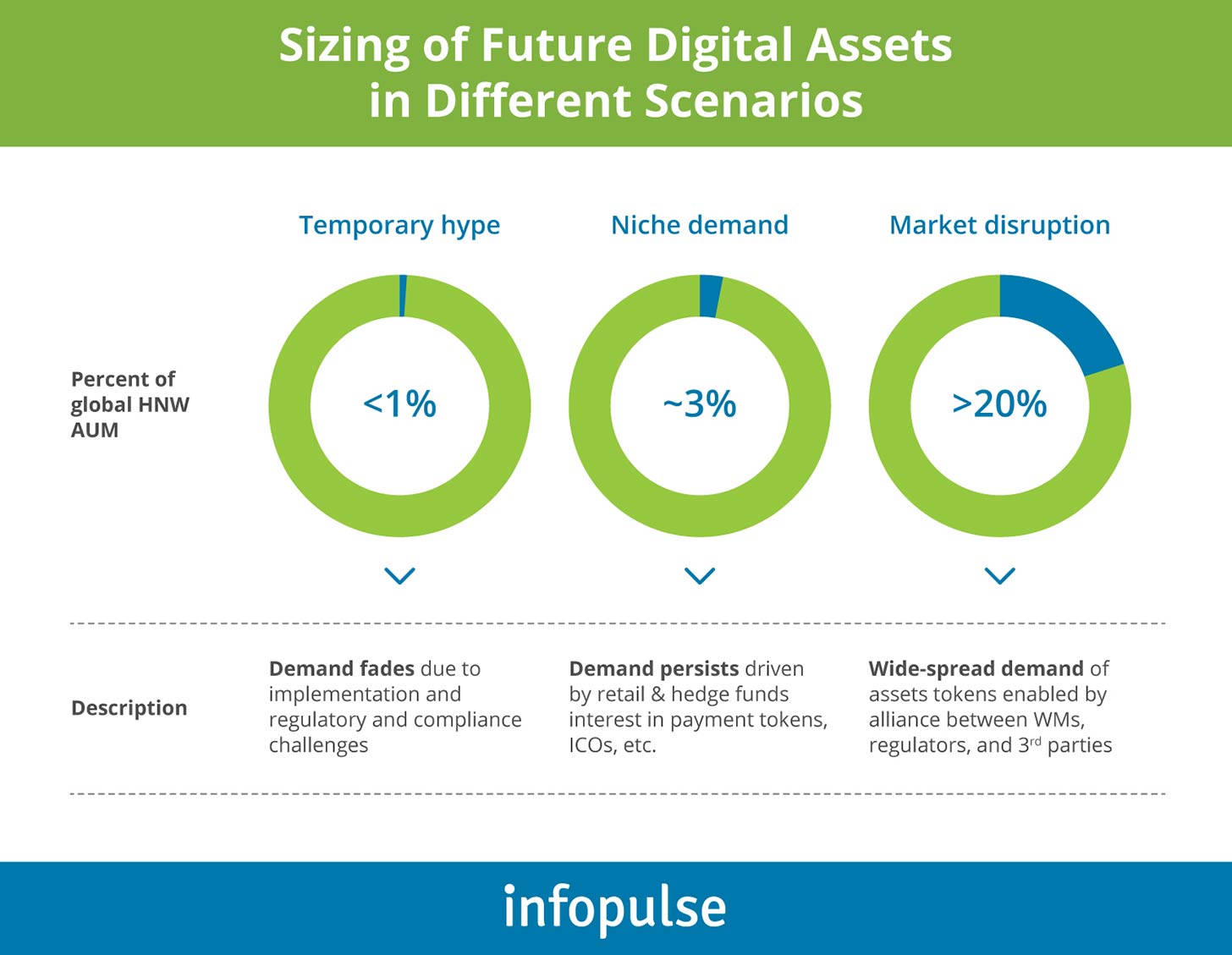

The swiftest way to capture a new market is to go after the lowest hanging fruit. When it comes to wealth management, digital assets — cryptocurrency, asset, and utility tokens —

are a niche asset class HNW and in which UHNW investors are highly interested, though not well structured and developed as of yet, according to Oliver Wyman.

Digital asset investment is a largely underserved market segment both by incumbents and by existing online trading apps. Shamefully so, as a niche asset class, digital assets already represented a total market size of $194 billion as of April 2020. Furthermore, a Bloomberg-published survey found that over 80% of institutional investors see the appeal in holding digital assets, and 36% of them already purchased this investment class. In fact, the penetration of crypto-assets is particularly high among the financial advisor, high net worth individual, and family office segments, especially in Europe. An industry outlook from State Street also suggests that 69% of the largest investment firms plan to increase their allocations to the digital asset class.

Unicorn neobank Revolut says that the launch of cryptocurrency was one of the most profitable decisions for them up-to-date. Within three months after launch, the bank’s customer base increased by 70%, and by the end of 2019, Revolut users amassed over $121 million worth of crypto. At the beginning of 2021, Revolut saw a peak interest in digital assets with over 300,000 new digital asset investor sign-ups in 30 days.

While the surged interest in digital assets often corresponds with the volatile fluctuations in Bitcoin prices, even with moderate hype digital assets it can still drive significant returns for wealth management companies:

Neobanks are in a good position to provide customers with straightforward and beginner-friendly functionality for trading digital assets — something most traditional crypto trading desks fail to provide.

The Challenges of Launching a Digital Wealth Management Product

The wealth management market entices digital players with a growing pool of profits. However, not all digital banks rush to evolve in neobrokers as they are somewhat deterred by the following challenges:

- Extra compliance and AML requirements: While many global regulators provide favorable or “regulatory sandbox” conditions for fintechs, digital banks who plan to move into the investing or trading spaces will be bound by extra regulations. For that reason, some banks choose to integrate wealth management solutions from third parties, rather than develop a custom one.

- Data management: To deliver personalized wealth management and advisory services, neobanks will need a more robust and mature data management infrastructure to support large-scale data aggregation and big data analytics initiatives.

- Security: For neobanks to gain the trust of HNWs clients, they need to up their cybersecurity practices — both customer-facing (e.g. introduce biometrics security) and internal facets (e.g. improve protection against DDoS and DNS attacks).

To Conclude

The mobile banking industry is growing more mature year-over-year. Early adopters grow more accustomed to using a portfolio of fintech tools to complement traditional banking accounts, while “strongly considering” types are ready to make the move to a digital-first service provider, especially in the wealth management space.

For neobanks, the diversification into trading, investment, and asset management can greatly help recoup the reduced profits from transactions, plus maintain a steady growth of monthly active users.

Contact Infopulse team to further discuss how your product can be enhanced with advanced big data analytics and machine learning capabilities to enable digitized wealth management services.

![CX with Virtual Assistants in Telecom [thumbnail]](/uploads/media/280x222-how-to-improve-cx-in-telecom-with-virtual-assistants.webp)

![Generative AI and Power BI [thumbnail]](/uploads/media/thumbnail-280x222-generative-AI-and-Power-BI-a-powerful.webp)

![AI for Risk Assessment in Insurance [thumbnail]](/uploads/media/aI-enabled-risk-assessment_280x222.webp)

![Super Apps Review [thumbnail]](/uploads/media/thumbnail-280x222-introducing-Super-App-a-Better-Approach-to-All-in-One-Experience.webp)

![IoT Energy Management Solutions [thumbnail]](/uploads/media/thumbnail-280x222-iot-energy-management-benefits-use-сases-and-сhallenges.webp)

![5G Network Holes [Thumbnail]](/uploads/media/280x222-how-to-detect-and-predict-5g-network-coverage-holes.webp)

![How to Reduce Churn in Telecom [thumbnail]](/uploads/media/thumbnail-280x222-how-to-reduce-churn-in-telecom-6-practical-strategies-for-telco-managers.webp)

![Automated Machine Data Collection for Manufacturing [Thumbnail]](/uploads/media/thumbnail-280x222-how-to-set-up-automated-machine-data-collection-for-manufacturing.webp)

![Money20/20 Key Points [thumbnail]](/uploads/media/thumbnail-280x222-humanizing-the-fintech-industry-money-20-20-takeaways.webp)