![API as a Product in Banking [banner]](https://www.infopulse.com/uploads/media/banner-1920x528-business-opportunities-of-api-products-in-banking-and-finance.webp)

Business Opportunities of API as a Product in Banking and Finance

So, what is an API for modern banking and finances? Companies that are growing or go through a digital transformation see APIs as central to new business logic. It is a mechanism to create value and exchange it between different businesses.

In this article, we will track the evolution of APIs from a tech tool to a business asset and uncover the unique opportunities of the API-as-a-Product model in modern banking.

The Evolution of API: from Middleware to a Product

In simple terms, API or Application Programming Interface is a set of definitions, instructions, and protocols to build and connect software. API connects two programs, exposing the select business or operational value of one with the other.

APIs establish a connection between systems and enable data access, allowing the monitoring of users and their activity. Well-designed APIs increase security and simplify back-end design for developers.

APIs are sometimes considered as contracts, with documentation representing an agreement between parties. When a client sends a remote request structured in a particular way, the server's software will respond by the preset rules.

However, the app-to-app contract model is no longer the only way to use APIs. The world of API has evolved far beyond this traditional "one program speaks to the other" operating mode. Instead, modern APIs are managed so that they can integrate multiple systems, both inside and outside the organization.

An API may exist either as a primary offer or as a separate product in the company’s business model. For instance, the API may be a premium feature if a business is built as a physical product or a Business-to-Business (B2B) service. At the same time, the API-first business strategy has become a primary approach for many new companies.

What Is API-as-a-Product in Banking?

The shift mentioned above resulted in a new paradigm for thinking and designing the API – API-as-a-Product. An API is placed at the very core of the business logic and now generates the most value for both business and customers. For API-as-a-Product solutions, the API is more than just the method to deliver data. It is an actual product that caters to the customers’ jobs-to-be-done.

API-as-a-Product is almost equivalent to an API-driven Software-as-a-Service (SaaS), where the API feeds the SaaS and the business logic surrounding it. API serves as a product for this software distribution model.

API products can be considered as a progression of the B2B approach: instead of creating custom offerings for specific instances, API-as-a-Product means: “Here is the functionality we offer, and it’s up to you how to use in your product”.

This paradigm is in alignment with the microservice movement. Instead of creating a single, catch-all solution attempting to cover a range of possible use cases, companies develop scalable frameworks that allow creating more fragmented solutions, responsible for fulfilling specific customer needs. It is a simple concept – why attempt to resolve each use case when you can create a series of low-level tools helping the problem owner to find a solution? As a result, developed solutions are more tailored to the desired outcome and more flexible to changes in the external environment.

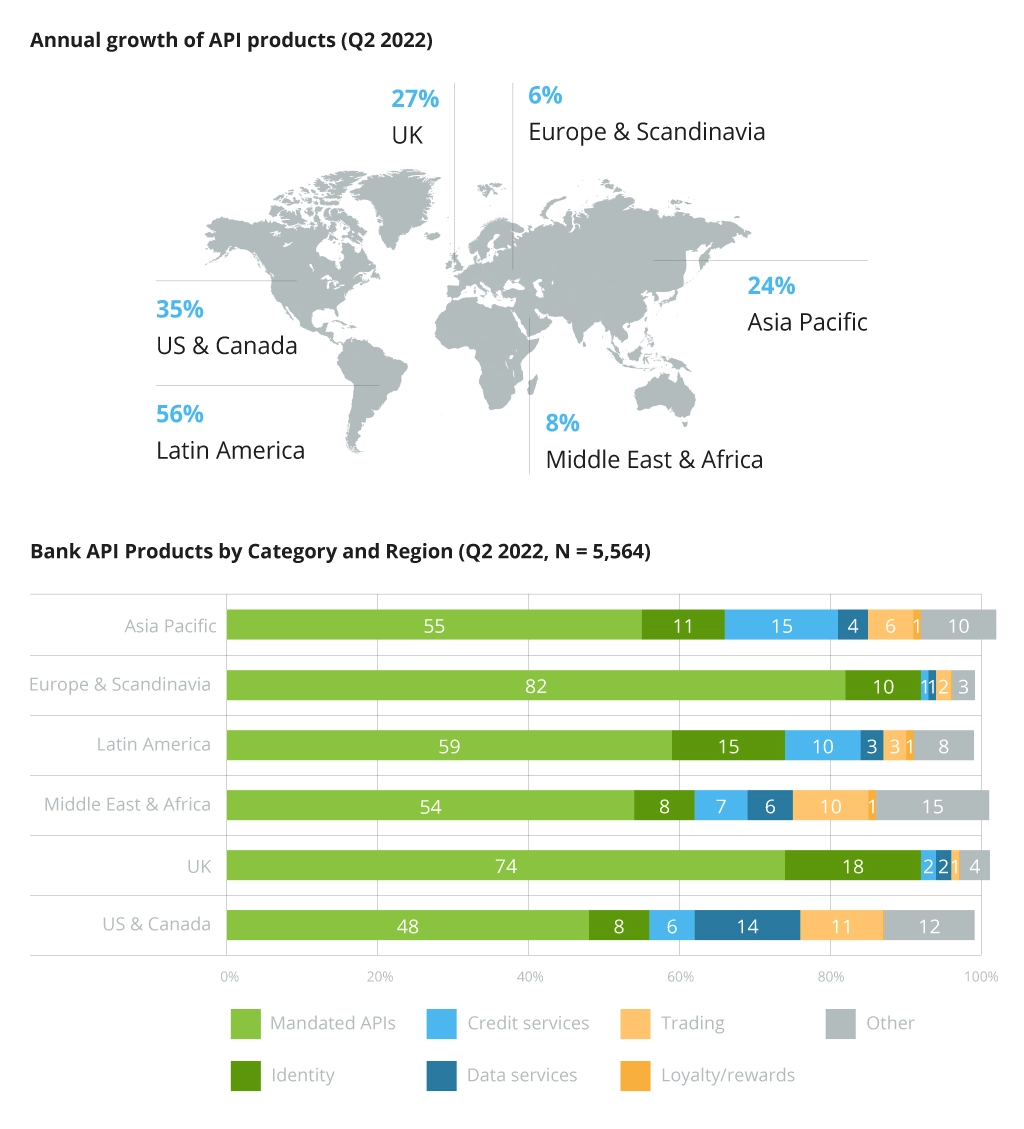

The number of API products for banking continues to grow stably, showing a 15% global increase in Q2 2022.

Annual Growth of Bank API Products by Region

The “API-as-a-Product” concept fits today’s transition of banks from the monolithic configuration to a more customer-centric, ‘service broker’ approach. It empowers banks with new business models and use cases, including:

- Bringing traditional financial services to the Web and mobile devices, such as online banking for accessing account information, transfers, bank product information, rates, biometric login, and others.

- Extending bank services to trusted partners. For instance, delivering digital payments, transfers between organizations, account information, and transitions from third-party applications through partners.

- Fostering new third-party connections through bank-led or partner-led loyalty programs, peer-to-peer lending with a bank as a clearing house, or a bank as authentication service.

- Leveraging new technologies, such as blockchain, big data/data science APIs for real-time market information, capital flows, customer experience data analysis, and more.

The new use cases create potential additional value for existing businesses in finance and give rise to new startups with an API-first business strategy.

Business Opportunities of APIs

The key drivers of developing API platforms and API products are increasing customer demands and new regulations. Yet, this move may result in even more opportunities and benefits.

First of all, API products drive business growth. Financial enterprises use APIs to connect with other businesses and consumers to increase the customer base or expand the range of services and benefits for existing clients with new services. They also streamline data transmission between companies to get meaningful insights about customer behavior and the marketing performance of different products.

Creating API platforms allows aggregating all services in one platform to create a one-visit experience for consumers, reducing the number of touchpoints to satisfy their needs. API-centric strategies in finances open new partnership opportunities to conquer the market outside the industry by creating value-added products to meet the growing customer expectations. For instance, numerous retailers adopt the Buy Now Pay Later option to improve customers’ purchasing power and boost sales. A bank can become a preferred partner for customer payment services for other businesses, using its high-quality and easily integrated API products.

Moving from a monolithic to a modular microservices architecture for API development, financial institutions significantly accelerate time to market, designing and delivering new services more quickly. It also helps future-proof the IT infrastructure thanks to the ability to react rapidly to new market trends and regulations. In this case, troubleshooting and maintenance also significantly reduces time and resources, decreasing the TCO of the provided products.

APIs strengthen commercial relationships with customers and increase their satisfaction through up-to-date service offerings and streamlined end-user experience. With all the benefits mentioned above, adopting an API-driven approach has become one of the leading directions in banks’ digital transformation.

The State of Financial API Products Market

There are many examples of financial services built with financial APIs on the market, including peer-to-peer lending marketplaces, used-car payments platforms, or industry-leading rewards platforms. The growth of API products in finance has been significantly increased within the open banking initiative. It allows securing data exchange between banks and third-party financial service providers. Under the hood, they operate with external APIs. Here are some examples of API products:

- Kiva: This non-profit organization enables people to provide investment loans to entrepreneurs globally. Kiva APIs give users programming access to the person-to-person micro-lending website, including functions to retrieve data about loans, borrowers, lenders, media, partners, and more.

- 2Checkout: an international payment system that allows transactions using Visa/MasterCard bank cards, or PayPal. API optimizes recurring cash flows across channels by making the back-end complications easier in modern digital business.

- Figo API: connects hundreds of banks and payment service providers through a standard interface. This API allows you to access your transaction history, initiate payments, and get notifications about changes such as incoming transactions, and others.

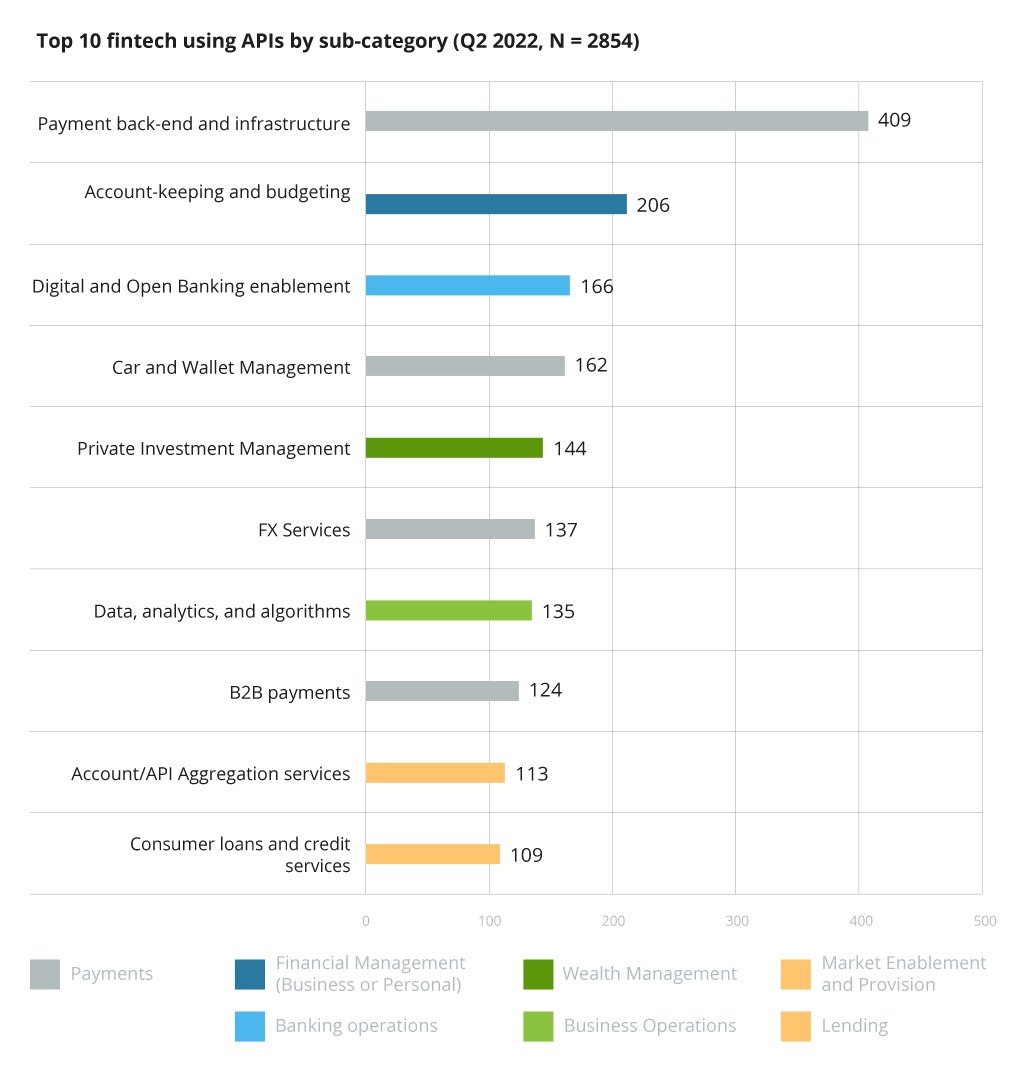

Open banking also extended business capabilities for fintech that now offers diversified API-enabled products led by payment back-end and infrastructure solutions.

Top 10 Fintech Using APIs

The growing adoption of open banking and banking API products influences the customer experience. According to an Onbe survey, 74% of consumers prefer digital payment methods over traditional ones, and 65% believe digital payments are more secure. 32% of surveyed respondents plan to use cash and checks less or completely refuse to use them over the next year.

Bank customers are actively moving to digital experiences that create advantageous conditions for new banking APIs appearing on the market.

Monetization of “API-as-a-Product”

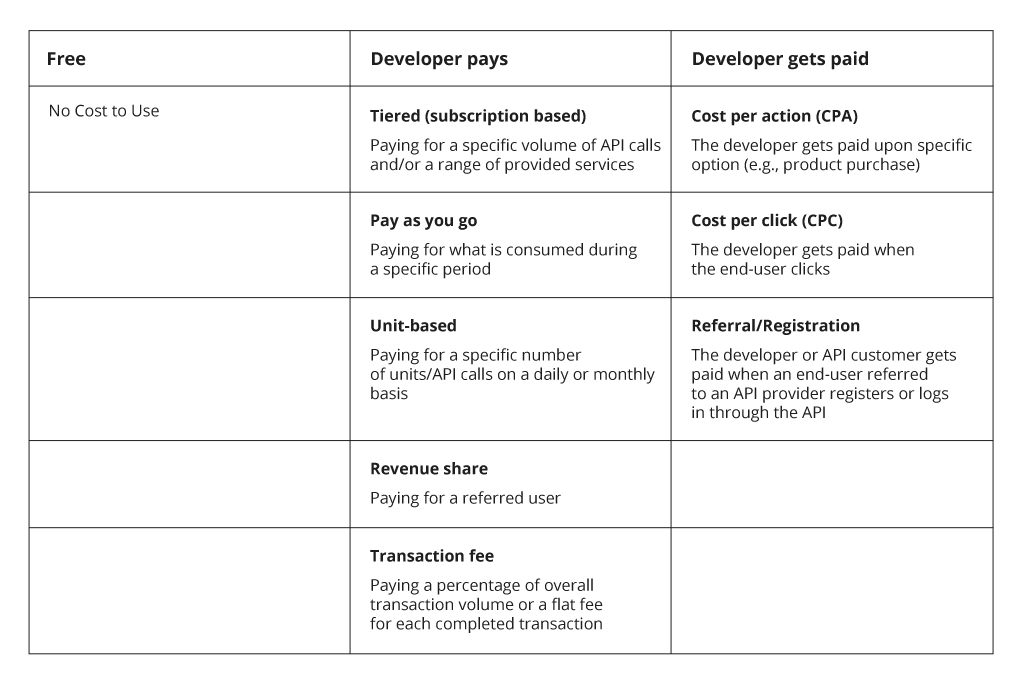

API banking products can be monetized in various ways. Some charge per integration or a certain amount of data transfer. Others might charge a portion of revenue or utilize subscription models. There are many banking APIs that provide a free level of service. This way, anyone can sign up for API and try out its demo.

Having a free tier (basic functionality available for free, full pack of features for a limited period, certain amount of data transferred for free, etc.) for API is essential. It allows potential partners to see if API is a good fit for their workflow. The most popular pricing models for API products in finance include the following:

- Tiered. Developers or API consumers can subscribe for various pricing levels based on data volume, the number of API calls, or the range of services provided.

- Pay As You Go. Developers or API consumers pay for what has been used – no minimums, no tiers (flagfall fee). It is usually billed periodically per API calls made.

- Revenue Share. In this model, API acts as an agent to help sell a provider’s product/asset. The API consumer or developer is paid a fixed fee or percentage of the transaction. In this model, the payment can also be made for every end-user referred to an API provider.

There are four primary groups of stakeholders for an API-as-a-Product: API providers, API customers, API developers, and end-users.

- API providers build, expose, and operate APIs. They are the API Product sellers who have a value proposition for a target market.

- API customers decide to buy API to use it in their own products. They are the Buyers of the Product, who are interested in the business value that the API brings on board.

- API developers or API consumers develop apps that use APIs. They are the Users of the Product, who need to ‘Get a Job Done’ and are interested in the product's functionality.

- End-users do not directly use APIs. Instead, they use APIs-enabled features in the app that is developed by the API consumer and provided by the API customer.

The entire range of available methods of API monetization is represented below. The payment options are categorized based on the direct (developer pays) or indirect (developer gets paid) pricing.

API Product Pricing Taxonomy

Banks actively experiment with new API-centered business models, primarily monetizing their API programs through partnerships and revenue sharing. Established financial institutions also develop partnerships with startups by offering funding and mentorship for early stages of product development or by acquiring fintech companies to fuel rapid API development.

Another popular business model among banking API providers is offering the partner's end-users white-label financial services – Banking-as-a-Service (BaaS). Banking giants like Banco De Brazil embrace an open ecosystem approach and offer API marketplaces. The company develops two directions of its API program to ensure compliance and build new revenue streams. Part of APIs is publicly available on the developer portal, while others are only for private use by selected partners.

Another example of BaaS API-based solution is Infopulse’s Mobile Banking App White Labeled for 10+ Nordic Banks. The solution provides instant and secure access to banking services online through native iOS and Android applications. Thanks to customizable, modular structure, the product was successfully adopted by numerous Nordic banks.

Final Thoughts

According to a famous saying in Silicon Valley, “There are only two business models – bundling and unbundling”. In 2022 and further, we are definitely in the era of unbundling, empowered by the API mindset. The transition from considering API as a middleware to an "API-as-a-Product" gave businesses new opportunities for digital transformation and opened new sources of added value. Providing API products to others is a proven way to extend financial services to new audiences and extend cross-industry partnership connections.

Infopulse has been providing the full range of digital services for the Banking and Finance industry empowering companies with the latest technological advancement. Our custom software development experts have vast experience designing solutions for omnichannel banking, loan management, open banking & PSD2 compliance, banking security, and infrastructure optimization. We are happy to assist in upgrading your financial enterprise and opening new business perspectives with reliable and secure API products.

![CX with Virtual Assistants in Telecom [thumbnail]](/uploads/media/280x222-how-to-improve-cx-in-telecom-with-virtual-assistants.webp)

![How to Build Enterprise Software Systems [thumbnail]](/uploads/media/thumbnail-280x222-how-to-build-enterprise-software-systems.webp)

![Super Apps Review [thumbnail]](/uploads/media/thumbnail-280x222-introducing-Super-App-a-Better-Approach-to-All-in-One-Experience.webp)

![IoT Energy Management Solutions [thumbnail]](/uploads/media/thumbnail-280x222-iot-energy-management-benefits-use-сases-and-сhallenges.webp)

![5G Network Holes [Thumbnail]](/uploads/media/280x222-how-to-detect-and-predict-5g-network-coverage-holes.webp)

![How to Reduce Churn in Telecom [thumbnail]](/uploads/media/thumbnail-280x222-how-to-reduce-churn-in-telecom-6-practical-strategies-for-telco-managers.webp)

![White-label Mobile Banking App [Thumbnail]](/uploads/media/thumbnail-280x222-white-label-mobile-banking-application.webp)

![Money20/20 Key Points [thumbnail]](/uploads/media/thumbnail-280x222-humanizing-the-fintech-industry-money-20-20-takeaways.webp)

![Deepfake Detection [Thumbnail]](/uploads/media/thumbnail-280x222-what-is-deepfake-detection-in-banking-and-its-role-in-anti-money-laundering.webp)