![Mobile Banking Trends [MB]](https://www.infopulse.com/uploads/media/banner-1920x528-mind-your-app-why-reinventing-mobile-banking-really-matters.webp)

7 Mobile Banking Trends that Matter These Days

What is the best way to translate your vision into products and services in a mobile banking app? How to appeal to your target audience and give your clients freedom to manage their finances anywhere at any time? In this article, we will go over the most requested mobile banking trends in the FinServ industry and help you master the art of mobile banking that will tick all the customer boxes. Are you ready to zhuzh up your mobile banking strategy?

What Factors Impact Customer Choice in Mobile Banking Apps?

To understand what makes a customer tick, let’s first have a look at the most important factors that influence the preferences of a regular suspect – a typical banking customer. Actually, at least three of them:

- Sharon, a mom of two teenagers, mentions that she chooses to manage her finances in an app because she can access the bank 24/7.

- Brian can’t be more vocal about paying his IOUs on his smartphone. He is a small business owner that has to pay his suppliers monthly.

- After having her wallet stolen, Ashley is very particular about her credit card information. She is glad to have full control over her sensitive data on the go.

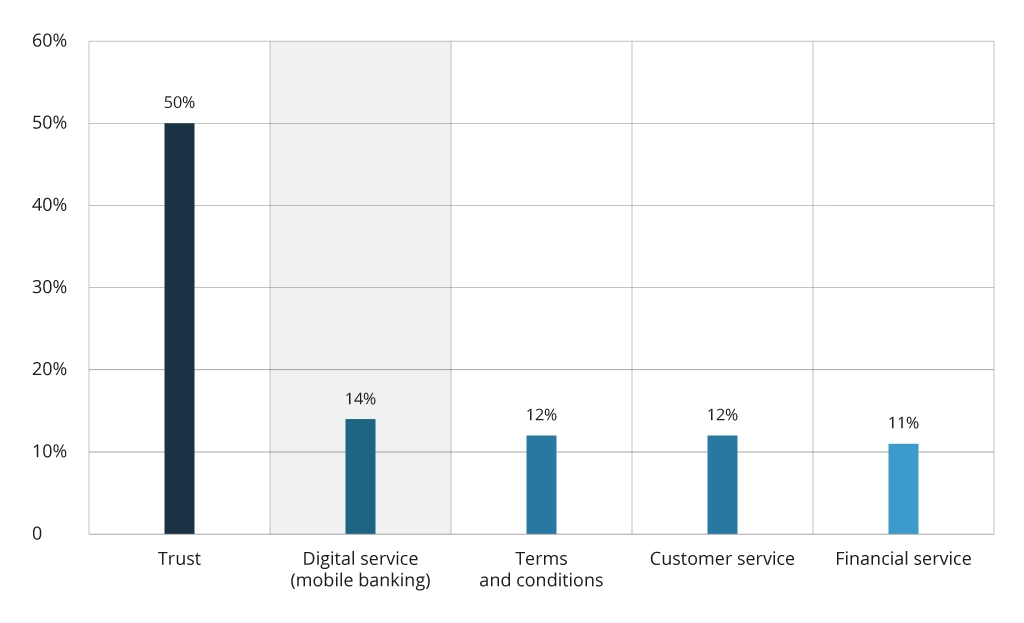

While trust is the most important when choosing a bank, what customers want next is the kind of comfort synonymous with mobile banking and digital access to all finances with embedded third-party products and value-added services. At least, that’s what the responders of Statista’s survey report, where 14% of users point their fingers at digitalization.

Thus, there is no escape from it. The reasons are many, and one of them being the fact that close to 90% of people admit they use their mobile banking at least once per month.

Another factor to mention is that banking is a very crowded marketplace today. Therefore, your financial products would better be new, original, and different: a user nowadays is very demanding, picky, and somewhat spoilt by too many options. So, customers pay more attention to the UX of the app and prefer those mobile applications that resonate with their lifestyle and needs.

For example, let’s look at the younger generation that is the keenest on customer-centric services on mobile. We have all heard about the wealth transfer from baby boomers to millennials. Thus, it’s crucial to have something to offer to those heirs; along with Gen Z, they are very reluctant to do anything off their smartphones. For them, the concept of meeting a bank clerk is alien, and one of the conditions for interacting with the bank would be doing it online. Perhaps, the reason is the younger generations are mobile-native. You can earn their trust and loyalty through mobile-first experience by talking to them in their own language – the parole of digital you ought to learn to offer ultimate CX. By establishing connections in their style, you are creating a community-like feeling they’re looking for, where FinServ offers full understanding of users’ identities and value systems. Tailored financial advice would reflect this comprehension as personalization is another element that factors into the equation.

The Importance of Knowing Your Customer Pains

Users of mobile banking often have a number of complaints. The essential here is to listen and hear them out; afterwards, you feed the dissatisfaction back into the pipeline when refining your mobile banking app. This opinion voicing is yet another opportunity for engagement with your customers. It’s also the ability to collect and analyze your users’ opinions to further enhance your banking services and the app UX. To better understand the universe of digital banking users, consider the most popular obstacles that keep users from embracing mobile banking:

- Complex UX: If the interface is far from intuitive, users might struggle to find the features they need. A complex, cluttered interface and confusing user journey can hinder on-screen experience too. Disappointed customers might want to consult a human customer service instead, which automatically makes financial services costlier. Ensure you refresh your app’s look and feel to appeal to users’ evolving habits.

- Privacy Concerns: Security of user personal data and financial information should be in-built in your banking app by design. Otherwise, any perceived vulnerabilities or data breaches can lead to complete mistrust and make users call it quits, choosing another bank. Furthermore, as a financial institution you might end up paying enormous penalties and fines on top of your damaged public image.

- Customer Support: Inadequate in-app customer support can leave users feeling left-out and not-cared-for when they’re in need of urgent help and some hand-holding. Since customer queries are often routine, many banks use chatbots to automate customer care.

- Authentication Struggles: Complex and frequent authentication processes, such as multiple security questions, OTPs, or even calls from bank managers to confirm the identity or operations can make the app less user-friendly, which is a turn-off for any busy user.

- Technical malfunctions, poor performance: Technical glitches, crashes, and errors can disrupt the user experience and prevent them from smoothly accessing their accounts on mobile and completing transactions online. It’s hard to disagree, that unstable applications can frustrate users, leading to poor mobile experience.

- Compatibility issues: Users might stumble across compatibility problems if the app doesn’t rhyme well with the operating system of a specific device which might lead to frustration, annoyance, and dissatisfaction with the app usage. The tip here is to develop cross-platform solutions in partnership with a trusted tech vendor, for example. Alternatively, you can use professional testing services to maintain and verify a large number of device-system combinations instead of doing QA on your own.

What Are the Most Impactful Mobile Banking Trends in FinServ?

Now that you’re aware of the heartaches of banking customers, it’s time to look at the other side of the coin. Let’s explore what FinServ on mobile is onto these days. See what trends prevail in mobile banking, so that you can smoothen your customer journey, attract new users and retain the existing ones.

1. Advanced Security

With an increasing emphasis on cybersecurity, mobile banking apps are packed with security features such as biometric authentication (fingerprint, facial recognition) and advanced encryption to ensure safe transactions and protect user data.

Case in point: Advanced identity verification and authentication with a 100% compliant GDPR eID platform can be one of the methods to elevate security. Self-sovereign identity solution offers full control over sensitive data and unified access across multiple services with selective disclosure.

As an option, you can consider multi-factor authentication to guarantee safe user experience and use it as a means of authentication to other channels, e.g., online transactions. Another tip: sometimes, checking your security vitals by performing penetration testing can help discover vulnerabilities before they snowball into a disaster. In general, the growing attractiveness of the financial service industry makes it a target for more and more hacking attempts. Therefore, professional security implementation, threat monitoring and testing best practices in partnership with a verified service provider is a far better option.

Case in point: Azure AD goes perfectly well with multi-factor authentication. A large energy sector player chose the Microsoft solution to address multiple security challenges and uplift the standards for user authentication. As a result of the transformation project, DTEK took its security to the next level to maintain business resilience amid COVID-19.

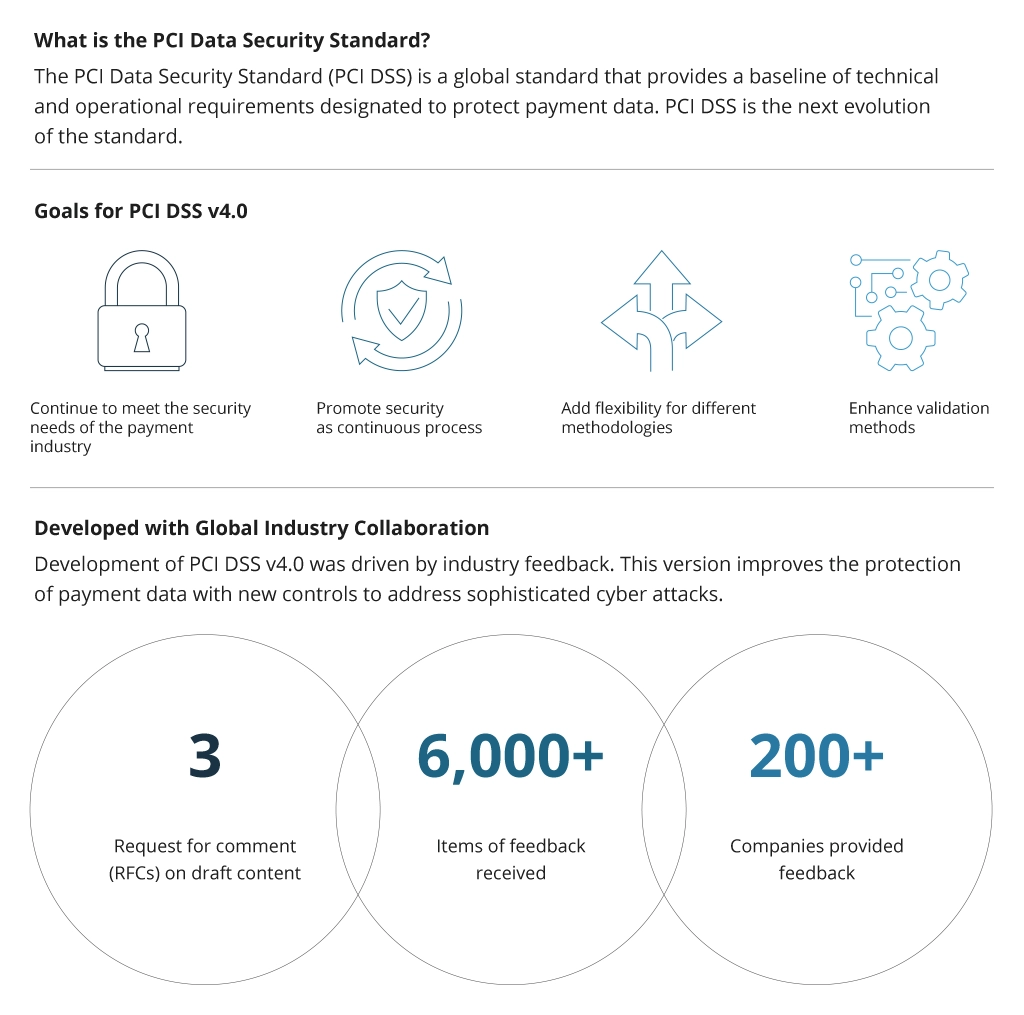

With the deadline on March 31, 2024, the Payment Card Industry Data Security Standard (PCI DSS) version 4.0 will put even more pressure on FinServ to ramp up security measures to protect payment data.

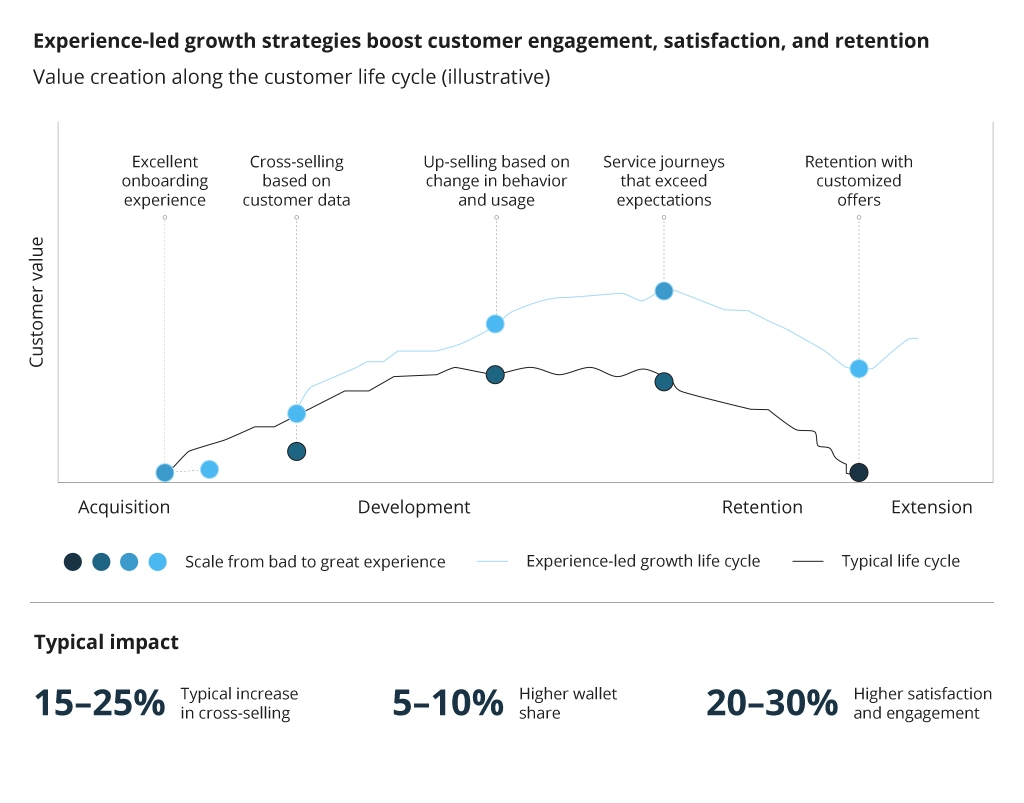

2. Personalization

Mobile banking apps made-to-order focus on delivering personalized experiences by offering tailored recommendations, insights, and financial guidance considering users' spending patterns and financial goals.

The point is to create long-lasting value throughout the customer journey. The result will speak for itself:

3. No Code/Low Code Development

This approach does not require complex coding skills or a team of developers and testers to be involved. Using no code/low code capabilities, you can add more functionality to core banking systems and speed up their time-to-market. No code/low code approach can enhance agility and help you to quickly respond to user demands on a budget.

Case in point: The second-largest bank in the Netherlands chose Power Apps to breathe new life into its heavy legacy applications. One of Robobank’s sales teams had long been having trouble figuring out how to link their mobile app and an on-premises CRM system. The solution was to use Power Apps, a low-code platform for building business apps, and their Azure on-premises gateway.

Using Power Platform to create the reorganization application that was necessary after the merger of retail and wholesale banking entities allowed the bank to reduce the time spent earlier on analytics from 3 weeks to 3 minutes.

Beyond that, the institution managed to reach a placement accuracy of 99.1% that was a way better KPI than it was pre-merger. In part, this was achieved because of automation. However, Power Platform played a pivotal role since it allowed engineers to develop applications that granted team leads and employees controlled access to the processes.

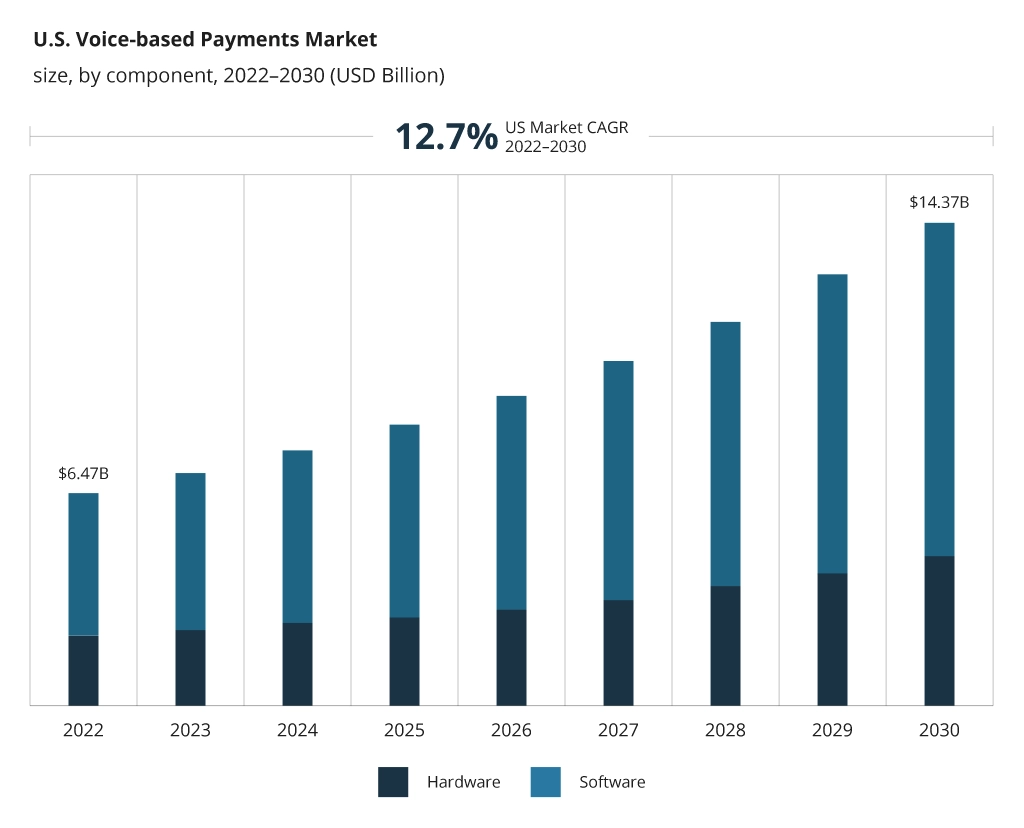

4. Voice Banking

Conversational banking is gaining traction as users can interact with mobile banking apps through AI-backed chatbots and voice recognition features, making transactions more intuitive and hands-free. The use cases of this technology in FinServ are many: from shopping to payments, voice banking opens new horizons of banking experience. The payments made through voice-banking tend to grow exponentially.

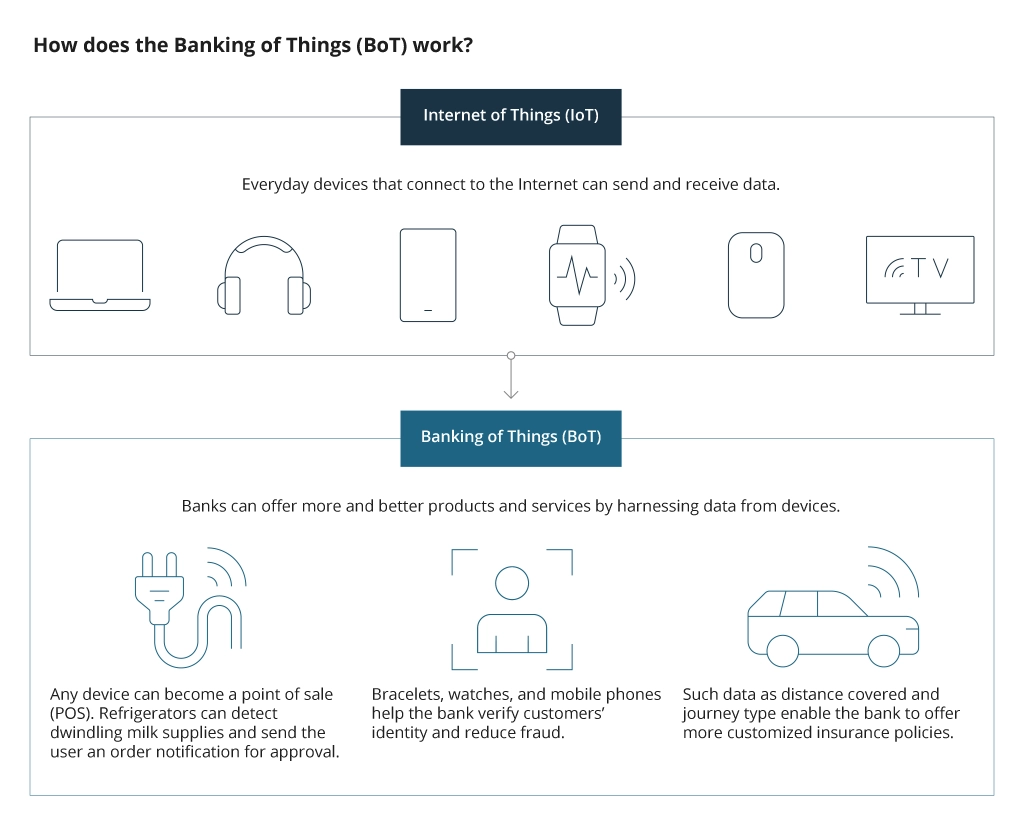

5. Internet of Things (IoT)

This technology in mobile banking is about features like smart payment systems, wearables for banking transactions, and integration with IoT-enabled devices that translates into a seamless banking experience. IoT solutions and the data you obtain from smart devices can help you segment customers based on their profiles, discover client spending patterns, create timely retention strategies based on ‘red flags’ that deviate from typical user journey, spot and typify credit risks as well as monitor discontent and return the feedback. You might be surprised, but BoT (Banking of Things) is already here and flourishing.

6. Digital-Only Banks and Blockchain

Digital-only banks earned the reputation of game-changers for their user-friendly interfaces, quick account opening, and innovative services. Beyond that, blockchain technology is being explored for secure and transparent transactions, and crypto-collateralized lending among others.

7. Modern UI and Easy-to-Use UX

Mobile banking apps are focusing on providing modern user interfaces with intuitive and easy-to-navigate designs to enhance user experience. Easy to find features, educational content to foster financial literacy, clear communication about ongoing personalized promos, and push notifications on partner offers can make users more interested in your app and as a result, improve cross-selling.

8. Messaging Integration

Incorporating messaging platforms within banking apps enables users to communicate directly with customer support, ask questions on the go, and receive prompt tips to solve the issues they experience. As a side effect, customer satisfaction grows, and you have their long-term loyalty as payback.

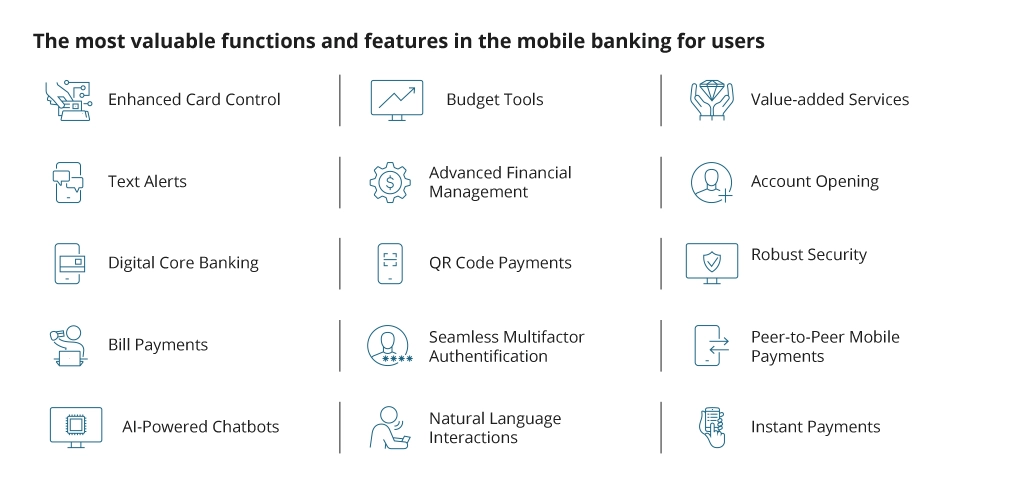

Mobile Banking Reboot: a Set of Essential Features to Deploy

Following the snapshots of your customer pain points and the prevailing market trends, we can now narrow down what features are essential to revive your mobile banking practices:

Perhaps unsurprisingly, enhanced card control is necessary to easily manage debit and credit cards through the app, including activating or deactivating them, setting spending limits, and receiving instant notifications for card transactions. Actually, mobile apps may replace payment cards with NFC payments capabilities, so the users will be able to leave home with only their mobile phones instead of with their wallets as well. These are simple truths and the bare minimum of a standard mobile banking app.

Value-added services like parking payments, travel tickets, charity, or general integration of other non-competitive financial services like insurance in the banking app would increase the number of user touchpoints and customer satisfaction giving lifestyle functions at hand an all in one, frequently used app. The factor is that for building and maintaining such integrations and app functions, you may need extra development efforts and time. Here’s where you can engage your external partner in mobile app development to pursue your goals.

After, you can step up the game with budgeting tools to help users track their spending, set budgets for different categories, and monitor their financial goals on the go. One more must-have is account opening directly from the app and an option to market and sell

products to logged customers: this would simplify the onboarding process and expand banking services without the necessity to venture to a physical branch.

Now imagine a customer journey. While a user browses for something in-app, you can suggest related services, cross-selling your offerings that hypothetically can match their search criteria – that’s why personalized promotional graphics should be a part of your mobile baking application too, and not only for the sake of keeping users informed of their financial activities or suspicious transactions. Security by design, including seamless MFA, іn mobile banking app is as essential as personalization or any other aspect that may influence the app usability and credibility. Seventy-four percent of European banking consumers said they feel secure using their bank’s mobile app. However, many still worry about fraud.

QR code payments come next as nice-to-have: they are quick and convenient, making transactions efficient and taking the friction out of the customer journey equation; as are peer-to-peer payments. Mobile banking apps facilitate easy P2P transfers between users who can enter a phone number instead of a bank account number, enabling quick payment settlements and splitting bills. Don’t forget to add this to your development backlog.

The cherry on top, of course, would be conversational AI, and it’s not only because S&P analysts are sure that the banks using it benefit from capabilities and efficiencies that sharpen competitive edge.

Bottomline

Mobile banking is changing at a galloping pace, altering its nature from one of the touchpoints in omnichannel strategies to something much more essential. The app takes the role of the most preferable interface customers value for its simplicity and round-the-clock reach. The benefits of managing financials on mobile are tangible both for customers and FinServ, who can now have a better understanding of their users as well as more opportunities for cross-sale.

![Banking Software Development [Thumbnail]](/uploads/media/thumbnail-280x222-software-development-out-of-the-box-vs-custom-vs-low-code-solutions.webp)

![API as a Product in Banking [thumbnail]](/uploads/media/thumbnail-280x222-business-opportunities-of-api-products-in-banking-and-finance.webp)

![Overview of Connected Banking and its Benefits [thumbnail]](/uploads/media/what-is-connected-banking-its-promises-and-benefits-280x222.webp)

![Low-code for Banking [thumbnail]](/uploads/media/thumbnail-280x222-low-code-benefits-use-cases-banking.webp)

![API Strategy for Banking [thumbnail]](/uploads/media/whys-and-hows-of-api-strategy-for-banking-280x222.webp)

![Open Finance vs Open banking [thumbnail]](/uploads/media/how-open-finance-extends-capabilities-of-open-banking-280x222.webp)