Forces Shaping the Future of the Banking Industry: Tech Trends 2024

- Banking & Fintech

- Innovations

- Data & Analytics

- Cloud & DevOps

- Digital Transformation

- Business Applications

- Cybersecurity

- Digital Experience

In this article, we will overview the primary disruptive forces that will reshape the banking and finance industry in 2024 and beyond. There are points for growth and generating value from the upcoming changes. Explore the practical ways to address industry challenges at the highest value for your business.

Technological Turbulence

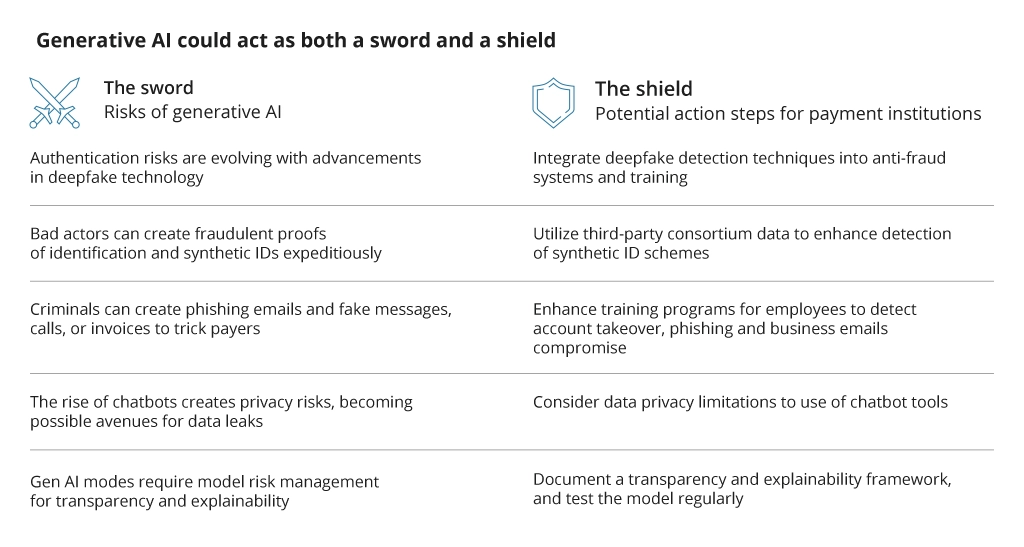

The banking sector in 2024 is adapting to a rapidly evolving technological landscape that brings both advancements and risks. One of the striking disruptive tech drivers is generative AI, which can improve workers productivity, enhance customer experience, and optimize costs simultaneously.

Traditional banks faced intensified competition from agile fintech startups offering innovative solutions like AI-powered personalized banking, decentralized finance (DeFi) services, and seamless mobile experiences. Their rise drives intensive collaboration between traditional banks and fintech firms to leverage each other's strengths and deliver better customer experience. As a result, banks receive innovations, while fintechs get access to a broader market.

Customers, on the other hand, reveal their readiness for new experiences. Juniper research shows that 3.6 billion people worldwide will become digital banking users by the end of 2024. What's more revealing is that almost 94% of these users are expected to engage in mobile banking every month.

Yet, generative AI adoption imposes certain risks. First, it may be challenging to determine the proper focus among all potential use cases and assess the risks toward the potential value:

Tech advancements require enhanced computing facilities that drive the transition to the cloud. The latest study from MarketsAndMarkets found that the global finance cloud market will grow to $268.1 billion by 2028, almost doubling from 2023:

The cloud provides on-demand scalability, perfectly fitting the dynamic market behavior and changing customer demand. Nevertheless, financial organizations face hurdles transitioning from on-premises to cloud infrastructure, increasing security and compliance risks. Cybersecurity became a paramount concern in the increasing digitization of the banking sector, leading to a surge in cyber threats and necessitating robust security measures.

Steps to Take

To balance the goals for growth with potential risks, it is reasonable to consider these further moves:

- Migrate legacy systems to cloud-based infrastructure for scalability and agility.

- Implement advanced AI algorithms to enhance customer service, risk assessment, and operational efficiency.

- Audit your IT infrastructure and strengthen cybersecurity measures.

- Deploy AI-driven fraud detection systems.

- Adapt to evolving market boundaries and explore cross-industry collaborations.

Overall, in 2024, the banking sector will adapt to a rapidly evolving technological landscape with all its benefits and risks, striving to maintain trust, security, and relevance in the digital era.

Greater Regulatory Pressure

The divergence in laws and policies, along with the lack of a coordinated, global approach to digital assets, cryptocurrencies, AI-related innovations, and data privacy, causes numerous regulatory risks related to:

- Consumer protection

- Product and organizational innovations

- Requirements for capital, reporting, and other activities.

There are more than 50 global and regional regulations, including the Basel III Accord, GDPR, AML, PSD2, KYC, SEC Regulations, and the newest EU AI Act - the world's first law to regulate the use of artificial intelligence.

In 2024, smaller and regional banks will face intensified regulatory pressures, mainly if they heavily concentrate their investment and lending portfolios or rely on specific deposit mixes. These banks will primarily focus on enhancing lending criteria and diversifying their balance sheets throughout the year. This shift aims to move away from risky assets like commercial real estate (CRE) loans and seemingly safe investments such as long-term treasuries.

Steps to Take

Banks face increasing regulatory pressure as technologies advance to provide greater transparency within the data and systems. On the other hand, technological advancements give resources to manage compliance risks effectively. You can meet the growing regulatory limitations and requirements with the following steps:

- Automatе risk-assessment questionnaires and models to manage risks effectively.

- Develop scenario analysis and stress test tools to simulate different interest rate scenarios, identify vulnerabilities, and proactively mitigate risks.

- Automate compliance workflows, which are typically highly rule-based and involve a series of approvals and checks, such as Anti-Money Laundering (AML), Know Your Customer (KYC).

- Develop real-time monitoring of compliance processes in the organization to reduce the risk of regulatory violations.

- Automate the balance sheet management process by optimizing the mix of assets and liabilities to align with the organization’s risk tolerance and interest rate outlook.

- Implement data analytics tools to monitor and respond to inflation trends.

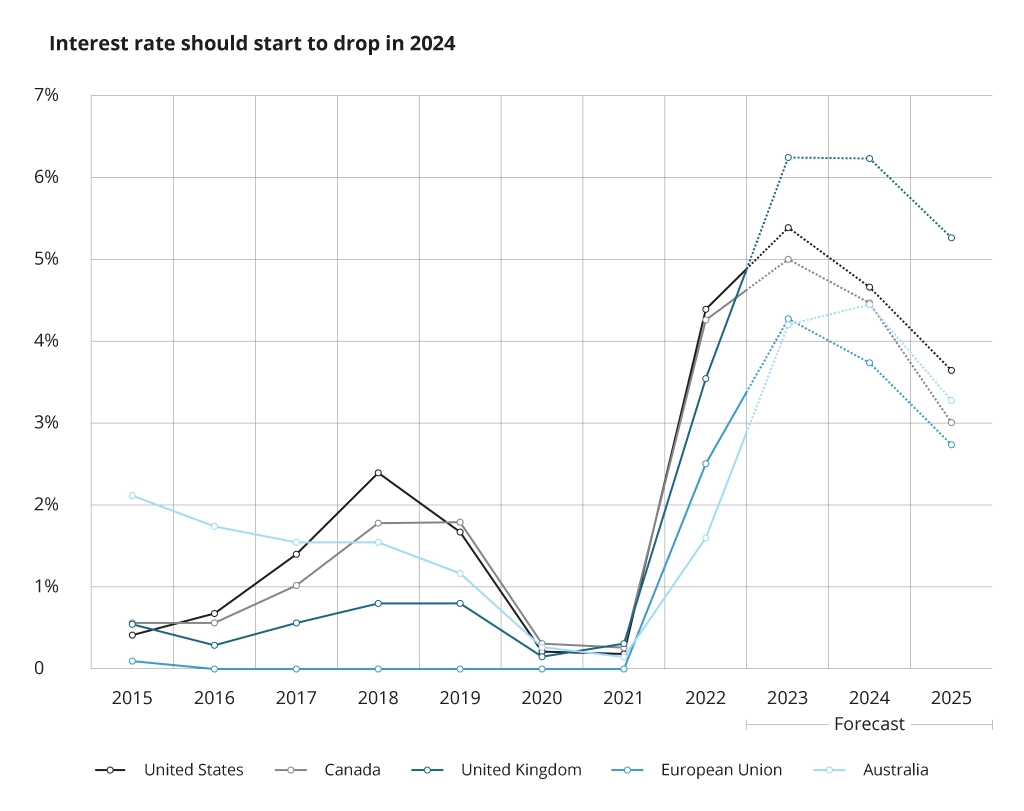

Higher Interest Rates and High Deposit Costs

In 2024, global inflation is expected to drop to 5.2% from 8.7% in 2022. The interest rates are also to decline in 2024 across all regions:

For banks, lowering interest rates will increase funding costs and tighten the margins. For US banks, the costs have risen more for regional and midsize banks. For example, in Q2 2023, the deposit costs for the largest banks were 2.2%, while for the smaller ones they were 2.5%. The same pattern is observed in other countries.

On the other hand, customers expect attractive deposit terms, and banks should find the right balance in deposit offers to stay competitive.

Steps to Take

Banks are able to finetune their rate policies with the help of technological advancements, including:

- Automating workflows for expense analysis to study operational costs, identifying inefficiencies, and optimizing spending in real-time.

- Automating vendor relationship processes: selection, negotiation, performance evaluation.

- Developing dynamic pricing models that adjust in response to market conditions, helping the organization to preserve margins.

- Automate profitability analysis by tracking the performance of different products, services, or client segments to identify areas for margin improvement.

- Automate cash flow forecasting to accurately predict liquidity needs and ensure funds are available when required.

- Develop scenario analysis and stress test tools to assess the impact of different liquidity scenarios.

- Automate communication with investors and reporting to retain investor's confidence.

- Implement custom solutions for personalized customer benefits to form a competitive advantage in the market.

Embedded Finance

Embedded finance adoption will continue to grow in 2024 as non-financial organizations tend to offer financial services to their customers.

Embedded finance is the process of integrating financial services into the customer journey. For instance, online stores, ride services, and social media include banking services on their platforms. Embedded finance often relies on the principles of open banking and open finance by utilizing APIs and data sharing to integrate financial services into external platforms. According to the latest predictions, the value of open banking payments transactions will exceed $330 billion globally by 2027 from $57 billion in 2023.

For banks, it is an ability to acquire additional customers through the Banking-as-a-Service (BaaS) model. Using APIs, banks can embed their products into partnering platforms.

Steps to Take

- Enable seamless financial services within non-financial products and platforms.

- Adopt API-as-a-Product model to open banking services for use from partnering platforms.

- Build partnerships with non-financial companies to expand embedded finance offerings.

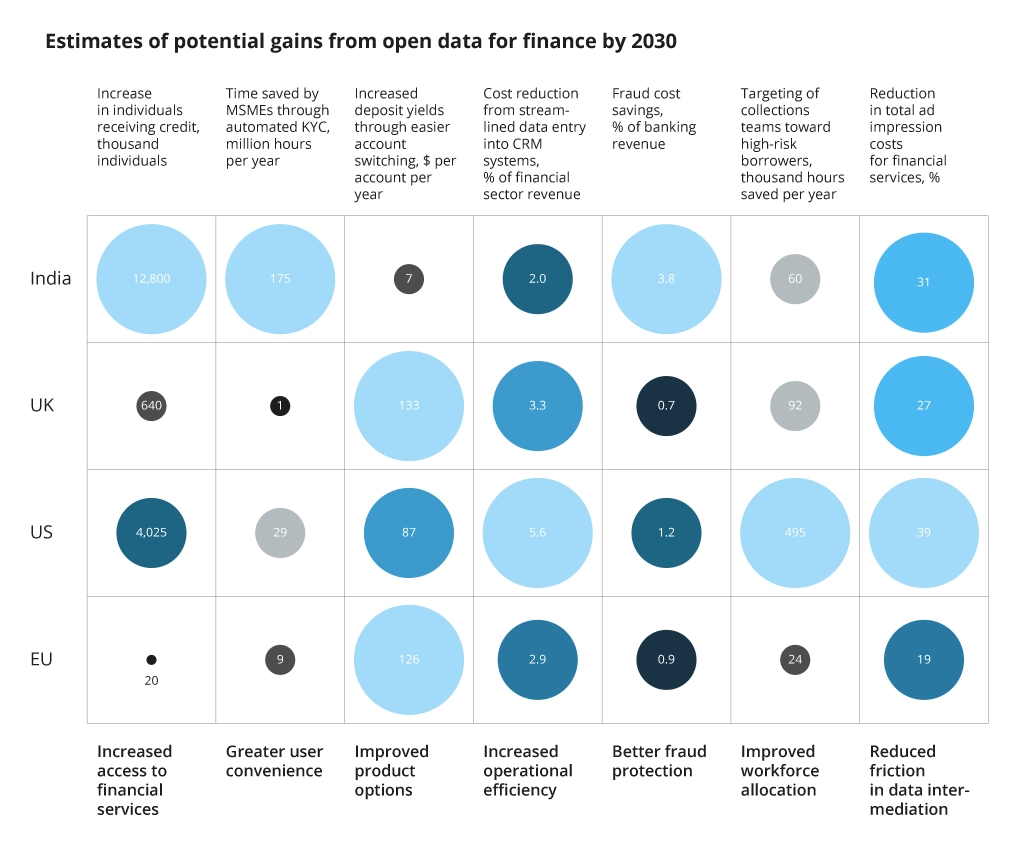

Open Data

The development of embedded finance and open banking logically pushed banks to embrace the open data concept. It implies that third-party providers like software vendors or fintechs access customer data via APIs to help consumers seamlessly pay within their shopping journeys.

Embracing open data in banking will stimulate innovation, improve customer experiences and satisfaction by giving users more control over their financial data. Fostering transparency and trust between financial institutions and their customers results in increasing organization profit. McKinsey’s analysis suggests that the broad adoption of open-data ecosystems can bring up to 1.5% of GDP in the EU, the UK, and the USA by 2030. It brings numerous benefits to customers and financial institutions:

The potential gains are balanced with the increasing risks related to data privacy and security, cybersecurity threats, regulatory compliance challenges, customer trust, operational risks, and misuse of information.

Steps to Take

Managing these risks involves implementing robust security measures, ensuring regulatory compliance, fostering transparency, and educating customers in the implications of sharing their financial data. It requires a balance between innovation, customer empowerment, and safeguarding data privacy and security by the following steps:

- Leverage open data for creating personalized and innovative financial products.

- Automate data consent workflows allowing customers to grant, revoke, or modify their consent for various data-sharing activities to give them a sense of empowerment and control over personal information.

- Develop customer data portals where individuals can access, view, and manage their personal information. For business process management, it will bring multi-channel data control, audit trails, data encryption, and security.

- Automate processes of customer data requests and inquiries while ensuring compliance checks.

- Develop a real-time reporting tool for customers to detail data-sharing activities.

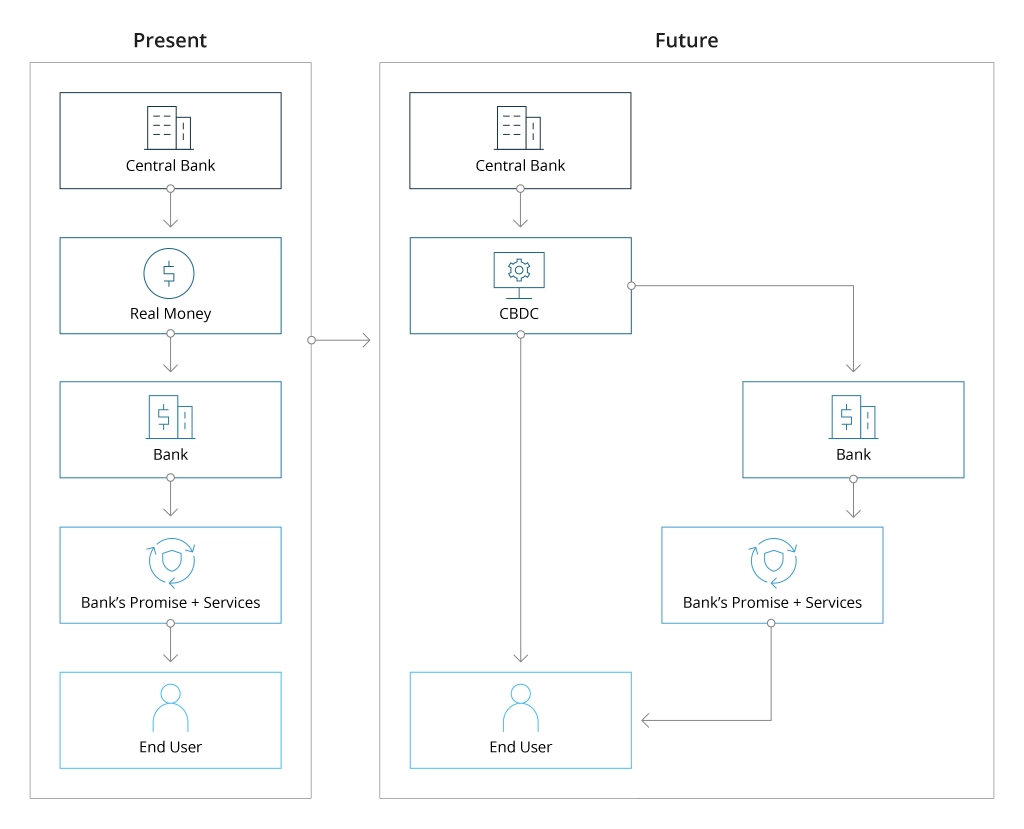

Digitization of Money

Central banks worldwide are exploring the potential of central bank digital currencies (CBDCs). China has already rolled out its 'e-yuan', EU officials are planning to release a digital euro by 2025, and the US's Federal Reserve is also considering issuing a digital currency.

The timelines for the earliest deployment of CBDCs worldwide are set for the mid-to-late 2020s. They combine traditional financial system stability with the benefits of modern digital technology. They aim to simplify payment, reduce transaction costs, and expand financial accessibility.

CBDC operates within a secure and transparent blockchain network to record all transactions securely. As a result, all transactions are documented on a decentralized ledger that ensures data integrity with the inability to modify or tamper with any information related to payments.

Still, CBDCs can potentially expose consumers and businesses to technology failures, privacy and transaction monitoring risks because CBDC holders will use both corporate and personal devices for transactions. In addition, businesses will have to comply with new regulations, yet forming a coordinated approach to regulating CBDCs requires time after their adoption.

Steps to Take

Depending on the pace of CBDC adoption, getting ready to embrace this revolutionary shift is vital. These steps are the ones to consider for the future technology adoption:

- Facilitate the integration of CBDC systems with existing financial infrastructure and prepare the appropriate changes in the business processes management for any integration workflows.

- Automate the real-time monitoring and validation of CBDC transactions to ensure compliance.

- Automate the creation and management of CBDC wallets for individuals and businesses.

- Automate currency conversion and ensure compliance with international financial regulations for cross-border transactions.

Digital Identity

Growing digitization in banking and finance and related cybersecurity risks propelled forward the demand for digital identity. According to the latest reports, the number of digital identity verification checks will reach over 70 billion in 2024, 16% more than the previous year's 61 billion. 37 billion from those 70 will be related to banking.

Utilizing biometric verification methods for online banking and other services is highly effective against different kinds of fraud and is also convenient for consumers. It saves time approving transactions, enabling new services, and other customer interactions.

Steps to Take

To strengthen competitiveness and enhance security, banks should consider the following:

- Implement digital identity solutions, custom-made or from identity verification vendors.

- Enhance customer authentication processes with biometrics and other digital verification methods.

- Prioritize user experience and convenience and design intuitive interfaces for verification processes that involve digital identity.

Fraud

Technological advancements work in both directions. They provide tangible benefits for banking services and operations but empower hackers with new tools for cyberattacks and fraud.

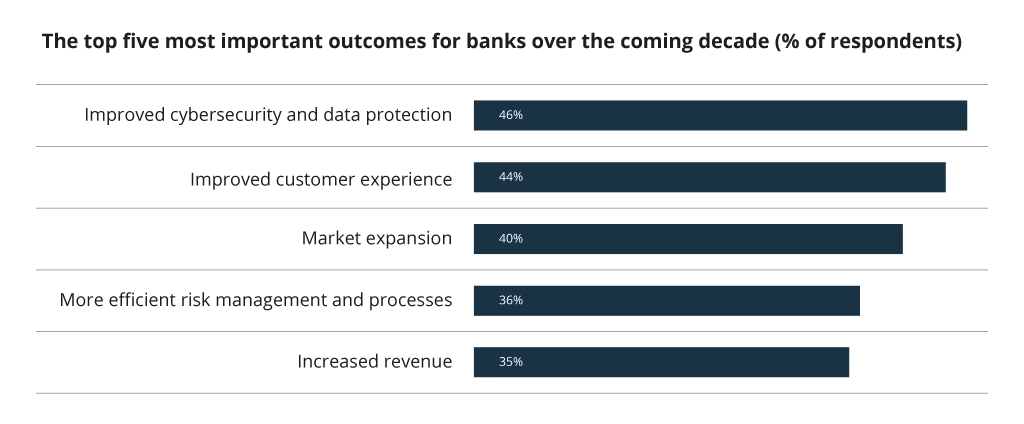

According to the latest survey by SAS, the increasing risk of cyberattacks is the third most important trend influencing the banking industry in the near future. Investing in cybersecurity and data protection capabilities is the top strategy 49% of executives consider the most effective for staying ahead or benefiting from the significant banking trends.

However, almost two in five respondents (38%) reported that their organization had not invested in data protection and cybersecurity capabilities. Nearly half haven't taken steps to improve data sharing between digital payment, fraud protection, and anti-money laundering functions.

Case in point: Infopulse implemented a complex solution to ING Bank Ukraine to assess cybersecurity vulnerabilities through Black Box and White Box penetration testing. As a result, the bank’s management team got the full report about the existing data security risks and recommendations for mitigating them.

Yet, most of these respondents mentioned that they plan to move in those directions in the next three to five years. A recent study conducted by Juniper Research indicates that the worldwide investment in AI-powered platforms for detecting and preventing financial fraud is projected to surpass $10 billion by 2027. This figure marks a significant increase from the approximately $6.5 billion spent in 2022.

Addressing the growing trend of fraud in the financial services industry is crucial to financial organizations for protecting customer trust, financial loss mitigation, regulatory compliance, and business continuity.

Steps to Take

- Deploy AI-driven fraud detection systems that can identify suspicious activities in real-time and flag potential fraud for further investigation.

- Automate fraud detection and response workflows to process all sensitive data flows effectively.

- Conduct fraud prevention training to educate employees on the latest fraud techniques and prevention methods. It increases awareness and ensures staff vigilance in identifying and reporting potential fraud.

Decarbonization

Commitment to sustainability and being eco-aware is an important factor customers consider when choosing a financial services provider. It impacts brand reputation, customer loyalty, access to capital, and can serve as a tangible competitive advantage on the market.

In 2021, the UN launched the Net-Zero Banking Alliance (NZBA), inviting banks ready to pledge to achieve net-zero carbon emissions across their lending portfolios by 2050. This alliance comprises 139 banks spanning 44 countries, collectively managing assets worth $74 trillion.

Transitioning to a green economy requires an extra $3 - $4.5 trillion of yearly investments globally. Banks and other financial organizations need to undertake strategic efforts to reduce their carbon footprint and minimize the environmental impact of their operations, assets, and lending activities.

Banks can invest in renewable energy projects to support sustainable energy sources and reduce reliance on fossil fuels. Using renewable energy sources for corporate buildings, optimizing energy consumption, reducing waste, and promoting telecommuting to reduce commuting emissions are the key steps to reduce the carbon footprint from internal operations.

Steps to Take

From the technological side, organizations can adopt innovations that directly and indirectly lead to net-zero carbon emissions. These measures include:

- Automated risk modeling and scoring to identify and mitigate environmental and social risks associated with loans and investments.

- Automated screening of investment opportunities against predefined sustainability criteria.

- Development of workflows to obtain green certifications or labels for financial products.

- Utilize AI and advanced data analytics to assess and support customer sustainability goals.

- Implement rigorous carbon accounting measures to accurately measure and report emissions across the bank's operations.

While reaching a zero-carbon footprint may be a long-term aspiration, banks can make significant strides by adopting technologies to shift towards green energy sources, reduce energy consumption, and foster a culture of environmental responsibility within their operations and investments.

Additional Value

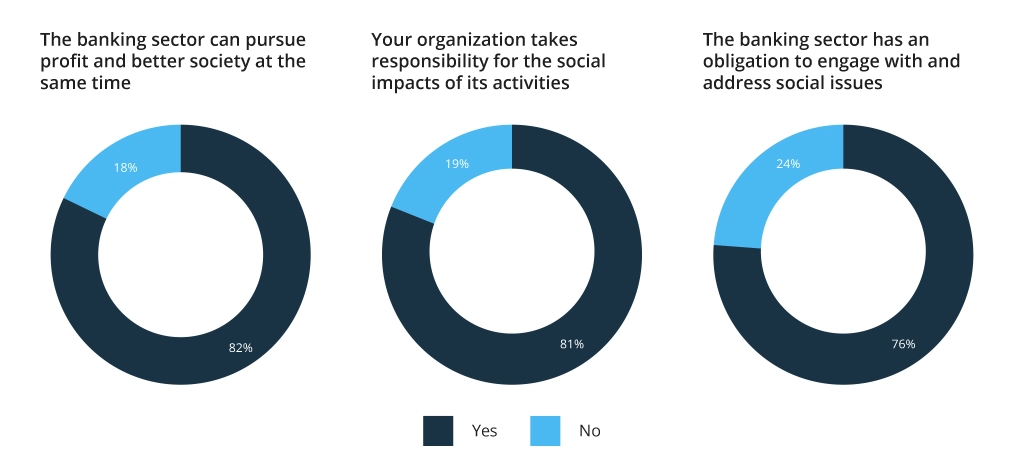

A Global Banking Survey Report by SAS reveals that 76% of banking executives believe that the industry is obliged to address the needs and issues of society, and 79% believe the industry should engage more in doing so. For 82% of respondents, financial organizations can simultaneously pursue profit and contribute to bettering society.

Modern customers tend to choose services from companies sharing corporate social responsibility, which results in higher financial stability for banks, according to recent research. CSR builds customer trust and positive customer outreach and boosts employee productivity, driving additional business value for the organization.

Steps to Take

The support for purpose-driven banking from C-level leaders is evident. The following measures help translate it into real action:

- Developing more inclusive and accessible products and services.

- Leverage technology to offer a more personalized, improved customer experience and higher employee satisfaction.

- Establish measurable ESG (environmental, social, and governance) commitments and goals.

- Build consumer awareness around ESG issues that the banks are engaged with.

- Increase transparency around the collection, use, and storage of customer data.

Conclusion

Aligning with modern trends in banking and finance brings sustainable business benefits. They help banks ensure resilience and competitiveness amidst the slowing global economy, dwindling money supply, swift adoption of new technologies, and growing regulatory pressure. The financial sector for the following years involves the following transformations:

- Technological advancements like AI and cloud computing provide opportunities for growth while improving risk mitigation.

- Customer’s digital readiness drives the need for seamless digital experiences, integrating banking into various sectors.

- Open data, central bank digital currencies, and digital identity have become crucial and demand robust security measures to address the ever-advancing fraud and cyberattacks.

- Purpose-driven initiatives and decarbonization amplify societal impact, customer trust, and business value.

For Infopulse, the financial services industry is one of the primary areas of expertise in technological advisory and custom software development. We provide up-to-date financial services, cybersecurity support, and intelligent automation, among many other services, to keep financial organizations evolving and progressing.

![Overview of Connected Banking and its Benefits [thumbnail]](/uploads/media/what-is-connected-banking-its-promises-and-benefits-280x222.webp)

![Low-code for Banking [thumbnail]](/uploads/media/thumbnail-280x222-low-code-benefits-use-cases-banking.webp)

![API Strategy for Banking [thumbnail]](/uploads/media/whys-and-hows-of-api-strategy-for-banking-280x222.webp)

![Digital Customer Engagement in Banking [thumbnail]](/uploads/media/a-complete-checklist-for-enhancing-digital-customer-engagement-in-banking-280x222.webp)

![Open Finance vs Open banking [thumbnail]](/uploads/media/how-open-finance-extends-capabilities-of-open-banking-280x222.webp)